Chapter 10 Economy and financial system

The plan was published in 2022. Some actions in the plan were amended in January 2025 as part of the Government's response to the Climate Change Commission's national adaptation plan progress report. These updates reflect changes in circumstances since the plan was published, and align with the Government’s climate strategy.

See the response and updated table of actions for more details.

Climate change is already affecting our economy. Its contribution to flood and drought from 2007 to 2017 cost $840 million in insured damages and economic losses.

Climate resilience is core to economic security. This chapter focuses on how we will adapt and build resilience to the economic and financial impacts of a changing climate. Some actions will also help identify new economic opportunities. This is part of Aotearoa New Zealand’s wider transition to a high‑wage, low-emissions economy that provides economic security in good times and bad.

E = Economy

EF = Economy and financial system

Taking action now can reduce long-term costs and bring opportunities.

Climate change is already affecting our economy. It is increasing existing risks, such as floods and droughts, and has resulted in sea-level rise. Between 2007 and 2017, the contribution of climate change to floods and droughts alone cost New Zealanders an estimated $840 million in insured damages and economic losses.*

The public sector, businesses, property owners and civil society need to take action to reduce the scale of the long-term economic costs, and seize the opportunities of a changing climate.

Central government will take action, for example, through legislation, regulation, information or funding to incentivise others to reduce their risk.

Local government will make decisions, for example, on land use or local infrastructure.

Businesses (including iwi interests) and private citizens exposed to climate risks will consider future climate impacts when making long-term decisions, such as where to locate, how to earn an income and what type of insurance to buy.

We have a way to go. For example, less than 10 per cent of firms have assessed risks to their business from a changing climate, and less than 20 per cent intend to take action to reduce their risks over the next five years.**

The actions in this chapter will support the public and private sector and private citizens to better understand and take steps to reduce their risks to climate change.

* See Estimating Financial Costs of Climate Change in New Zealand: An Estimate of Climate Change-Related Weather Event Costs [PDF, 1.3 MB]

** See the Business operations survey: 2021 [Stats NZ website]

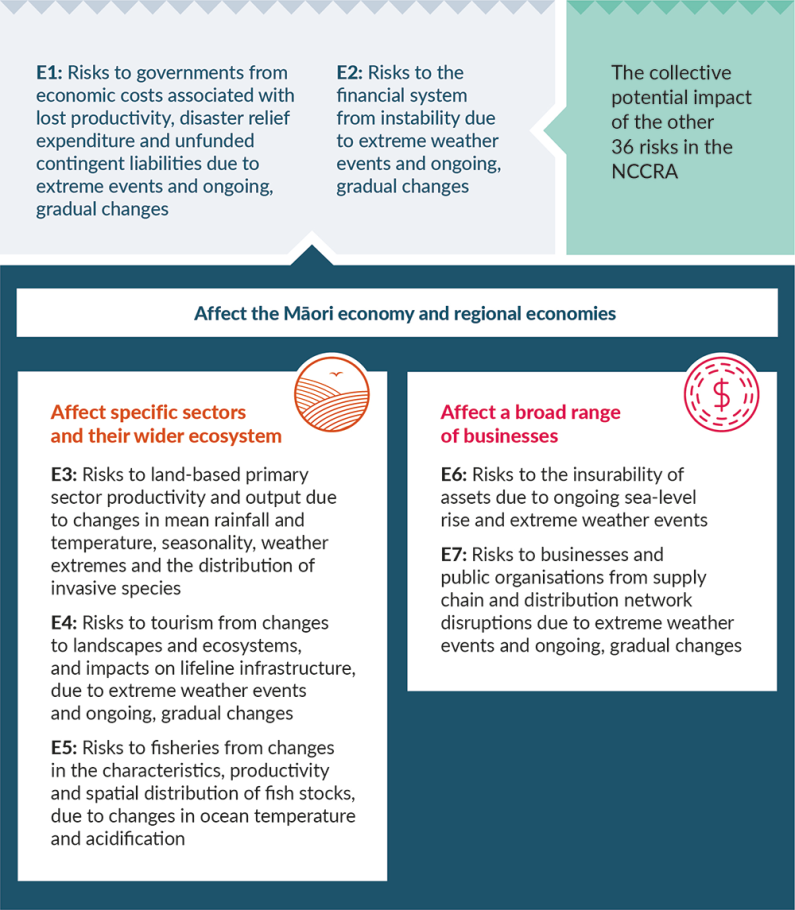

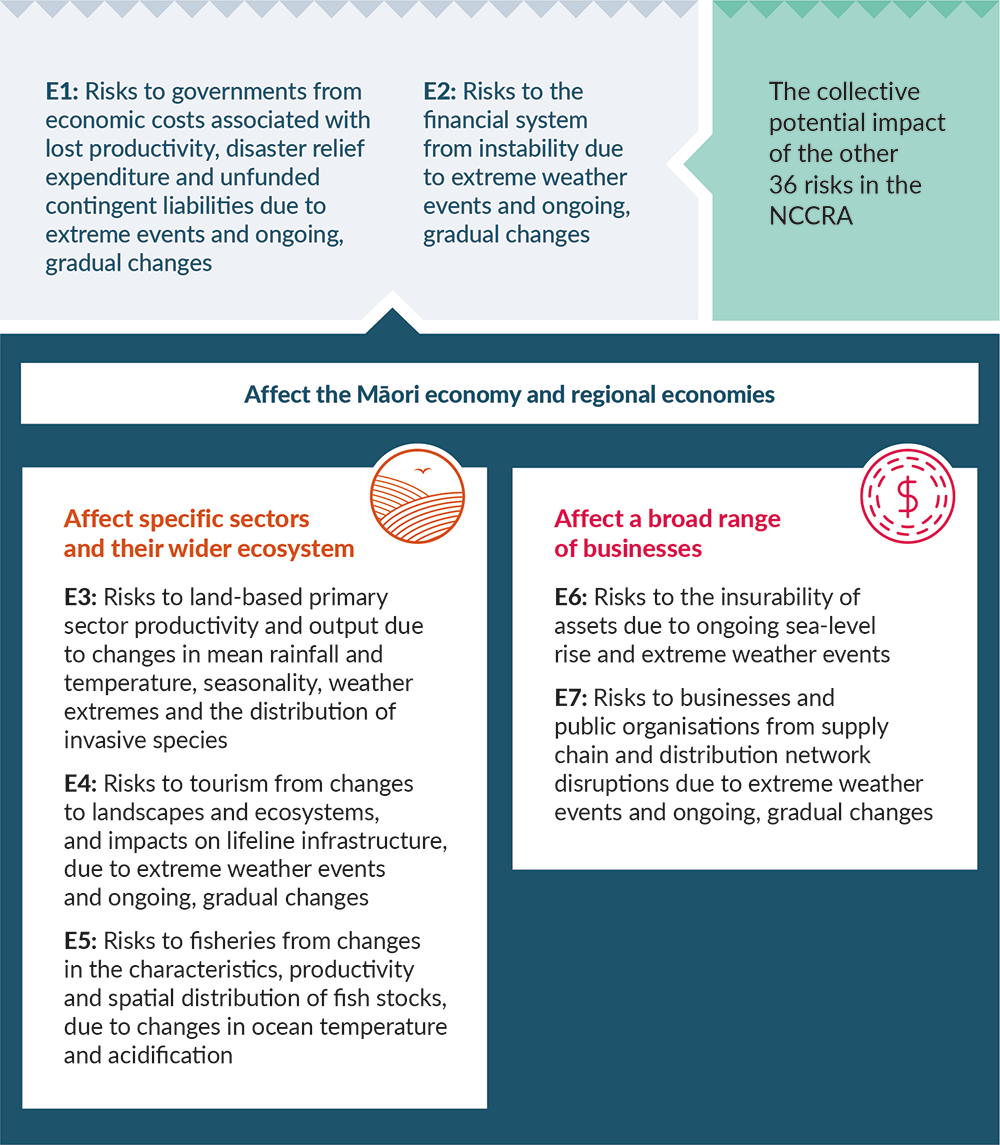

This plan addresses the seven economic risks identified in the National Climate Change Risk Assessment 2020. These will create flow-on effects on the economy – see figure 9 and the discussion on the following pages.

The collective potential impact of the other 36 risks in the NCCRA:

E1: Risks to governments from economic costs associated with lost productivity, disaster relief expenditure and unfunded contingent liabilities due to extreme events and ongoing, gradual changes.

E2: Risks to the financial system from instability due to extreme weather events and ongoing, gradual changes.

Risks E3 to E7 affect risks E1 and E2.

Affect the Māori economy and regional economies

Affect specific sectors and their wider ecosystem

E3: Risks to land-based primary sector productivity and output due to changes in mean rainfall and temperature, seasonality, weather extremes and the distribution of invasive species.

E4: Risks to tourism from changes to landscapes an ecosystems, and impacts on lifeline infrastructure, due to extreme weather events and ongoing, gradual changes.

E5: Risks to fisheries from changes in the characteristics, productivity and spatial distribution of fish stocks, due to changes in ocean temperature and acidification.

Affect a broad range of businesses

E6: Risks to the insurability of assets due to ongoing sea-level rise and extreme weather events.

E7: Risks to businesses and public organisations from supply chain and distribution network disruptions due to extreme weather events and ongoing, gradual changes.

The collective potential impact of the other 36 risks in the NCCRA:

E1: Risks to governments from economic costs associated with lost productivity, disaster relief expenditure and unfunded contingent liabilities due to extreme events and ongoing, gradual changes.

E2: Risks to the financial system from instability due to extreme weather events and ongoing, gradual changes.

Risks E3 to E7 affect risks E1 and E2.

Affect the Māori economy and regional economies

Affect specific sectors and their wider ecosystem

E3: Risks to land-based primary sector productivity and output due to changes in mean rainfall and temperature, seasonality, weather extremes and the distribution of invasive species.

E4: Risks to tourism from changes to landscapes an ecosystems, and impacts on lifeline infrastructure, due to extreme weather events and ongoing, gradual changes.

E5: Risks to fisheries from changes in the characteristics, productivity and spatial distribution of fish stocks, due to changes in ocean temperature and acidification.

Affect a broad range of businesses

E6: Risks to the insurability of assets due to ongoing sea-level rise and extreme weather events.

E7: Risks to businesses and public organisations from supply chain and distribution network disruptions due to extreme weather events and ongoing, gradual changes.

The risks to the economy set out in figure 9 will create the flow-on effects set out below.

Land-based primary industries, fisheries and aquaculture and tourism are Aotearoa New Zealand’s most exposed industries as they depend on climate-sensitive natural resources.* These three sectors and their manufactured products form a significant part of the economy and comprise over 60 per cent of exports.**

Failure of firms in these industries to adapt adequately would reduce their productivity and potentially their viability. Impacts would flow on to their suppliers and customers and to our export earnings.*** Climate-related impacts in other countries could also disrupt trade and influence demand for our goods and services.

* See the National Climate Change Risk Assessment Technical Report.

** The three sectors contributed about 62 per cent of export earnings for the year ended March 2020 (Stats NZ data on goods and services trade by country, and the tourism satellite account [PDF, 1.5 MB], both for the year ended March 2020).

Economic impacts will not be evenly distributed across Aotearoa. Many regional economies rely heavily on the three exposed industries. Economic activities in hazardous areas, such as low-lying land, will be further exposed. Failure to adapt could lead to business closures and job losses. This would have significant implications for workers and households, and, if widespread, could result in people having to leave some communities.

Māori are heavily invested in land-based primary industries, tourism and fisheries, which all have a significant Māori workforce.

Māori collectively own about 40 per cent of the fisheries quota, and have diversified interests across the sector, including catching, processing, marketing and food services. Māori also own 40 per cent of commercial forests. In 2018, gross domestic product (GDP) from Māori tourism was estimated at just over $975 million.*

Economic inequity means that some Māori businesses and workers have less capacity to adapt. Climate-related costs and disruptions could entrench those inequities. At the same time, Māori knowledge of sustainable practices and holistic economic models offer unique ways to adapt. If properly resourced, Māori can take a leadership role in adaptation.

* See Te Ōhanga Māori 2018: The Māori Economy 2018 [PDF, 17 MB]

Some assets could become uninsurable. This will create further issues if they are used as collateral for lending. The value of buildings exposed to coastal flooding could increase from $12.4 billion now to $26 billion for a sea-level rise of 0.6 metres, and $44 billion at 1.2 metres.*

Insurance retreat would likely reduce private and public asset values, making households and firms or public entities less able to invest in adaptation.

There are likely to be more insurance claims, greater damage repairs and higher premiums. Claims for extreme weather events hit a record $321.6 million in 2021, breaking the previous record set in 2020 at $274 million.**

* See Coastal Flooding Exposure Under Future Sea-level Rise for New Zealand [PDF, 3.7 MB]

** See Record Insurance Support for Communities – 2021 Extreme Weather Claims Exceed $300 M [Insurance Council of New Zealand website]

Local and global supply chains are critical to the functioning of the economy. Supply chains are disrupted by extreme weather (eg, flooding and power outages) and longer-term climate changes that reduce the supply of certain goods (eg, reduced global grain supply from prolonged droughts). Disruptions can range from the very local (eg, a washed-out road to a major tourist site), to major freight hubs, through to global distribution networks. The Intergovernmental Panel on Climate Change (2014)* suggests global climate impacts and their flow-on effects to our supply chains may be more significant to our economy than the direct impacts within Aotearoa.

Financial stability means having resilient banks, insurers and other financial institutions. It means we have a system that can withstand severe but plausible shocks and continue to provide the services we all rely on.*

There are two main ways that climate change challenges financial stability. First, the realisation of physical risks could lead to abrupt change in asset values (eg, extreme weather damaging residential housing or farmland or changing production outputs). Second, a disorderly transition to a low-carbon economy could also have an abrupt effect on value (eg, regulatory changes and legal challenges driving down value in emissions-intensive industries).

* See Financial stability report [Reserve Bank of New Zealand website]

In its 2021 statement on the long-term fiscal position, the Treasury modelled the impact of more frequent and severe storms and droughts.* The median impacts by 2061 appeared modest (net debt 3.77 per cent of GDP higher than baseline).

This analysis suggested the Government’s fiscal position was relatively resilient. However, these national impacts did not reflect the severe shocks felt by affected communities or local government entities. The fiscal impacts could be greater, given the analysis did not consider sea-level rise, non-linear or ‘tipping-point’ changes, or effects beyond 40 years.

* See Te Tirohanga Mokopuna 2021: The Treasury’s Combined Statement on the Long-term Fiscal Position and Long-term Insights Briefing [The Treasury website]

The Government may face lower revenue if tax revenue falls or if productivity or GDP reduce, and the costs to replace or repair its own assets increase.

Climate resilience is core to economic security.

The objectives and actions in this chapter focus on adapting and building climate resilience into our transition to a high-wage, low-emissions economy in a way that is fair, inclusive and upholds Te Tiriti o Waitangi.

This means an economy where:

The Government has identified two objectives for the economy and financial system.

|

Code |

Objective |

Explanation |

|---|---|---|

|

EF1 |

Sectors, businesses and regional economies can adapt. Participants can identify risks and take action. |

|

|

EF2 |

A resilient financial system underpins economic stability and growth. Participants can identify, disclose and manage climate risks. |

|

Actions to support a resilient economy and financial system are set out in the sections below. Chapter 3: Enabling better risk-informed decisions and chapter 5: Adaptation options including managed retreat also contain actions that are critical to supporting a resilient economy and financial system. These are:

A climate-resilient economy will support vulnerable New Zealanders.

The economic and financial impacts of a changing climate will not be evenly distributed. Fisheries, tourism and land-based primary industries are particularly exposed to climate risks.

To create equitable climate-resilient economies, we must address how regional economies, rural communities, Māori and workers and households with strong reliance on these sectors will also be disproportionately affected. Workers that are left with more insecure employment and displaced workplaces due to climate impacts need to be supported.

The actions in this chapter focus on adapting and building climate resilience in a way that is fair and inclusive by:

Timeframe: Years 1–6 (2022–28)

Lead agency: MOT

Relevant portfolio: Transport

Primarily supports: Objective EF1

Status: Current

This strategy will present a long-term and system-wide view of the freight system. Climate adaptation is being considered through the resilience outcome, to ensure Aotearoa New Zealand’s freight and supply chain system is resilient, reliable and prepared for disruption. This will inform investment by the Government, councils and private sector players.

The strategy looks across industries, sectors and modes to identify challenges and opportunities in the long term. This will lay the foundation for identifying any actions to reduce the risk of supply chain disruptions on businesses, industries and consumers.

The strategy’s equity and safety outcome commits the Government to ensuring that the transition to resilient supply chains is fair, equitable and inclusive. This means ensuring the Government is considering opportunities to support Māori, regional economies, businesses and workers to adapt to expected changes.

By the middle of 2023, the Government will have launched the New Zealand Freight and Supply Chain strategy.

Timeframe: Years 1–6 (2022–28)

Lead agency: MPI

Relevant portfolio: Oceans and Fisheries

Primarily supports: Objective EF1

Status: Current

The Government is progressing work on the Fisheries Amendment Bill, which includes several legislative changes to the Fisheries Act 1996. The aim is to strengthen and modernise Aotearoa New Zealand’s fisheries management system. The Bill sets tighter rules about what fish commercial fisheries must bring back to port and what they can legally return. The Bill also allows for more agile and streamlined decisions in response to changes in fish stock abundance, by enabling development of the pre-set decision rules.

These rules will allow adjustment of the catch limits, and other sustainability measures within pre-agreed limits, in response to change in abundance. This will allow for the system to be more responsive to the effects of climate change.

By late 2022, the Fisheries Amendment Bill will be passed.

Timeframe: Years 1–4 (2022–26) and ongoing

Lead agency: MPI

Relevant portfolio: Oceans and Fisheries

Primarily supports: Objective EF1

Status: Current

The Government’s Aquaculture Strategy sets objectives and actions to support Aotearoa in becoming a world leader in sustainable and innovative aquaculture. One of the strategy’s objectives is to support the industry to adapt to climate change.

Actions include: forecasting the effects of climate change on the aquatic environment and supporting actions for resilience; helping industry to transition to hatchery spat production; spatial planning approaches informed by climate change considerations to enable industry growth and adaptation; and the development of a comprehensive biosecurity approach.

By 2024, the Government will continue releasing implementation plans for the Aquaculture Strategy and reporting each year on the environmental effects of aquaculture.

Timeframe: Years 1–2 and ongoing (2022–24)

Lead agency: RBNZ

Relevant portfolio: Finance

Primarily supports: Objective EF2

Status: Current

The Reserve Bank of New Zealand (RBNZ) is taking action to help regulated financial entities identify and manage climate risks better. This includes:

By March 2024, the RBNZ will have climate change considerations increasingly integrated into its supervisory, stress-testing and policy work.

Timeframe: Years 1–6 (2022–28)

Lead agency: MPI

Relevant portfolio: Agriculture

Primarily supports: Objective EF1

Status: Current

This action will deliver a tailored extension programme for whenua Māori. This will support collectives of Māori landowners and agribusiness to take a te ao Māori approach to meeting their aspirations for their whenua in a productive and sustainable way. As part of the programme, landowners will consider how best to plan intergenerationally for the impacts of climate change on their whenua. It will extend the current pilot programme, which offers resources and support to Māori landowning collectives.

Timeframe: Years 1–6 (2022–28)

Lead agency: MPI

Relevant portfolio: Agriculture

Primarily supports: Objective EF1

Status: Current

This work will fund research and develop tools to support the agriculture sector to adapt to climate change better, measure emissions and mitigate land-use impacts on freshwater. It includes science extension and policy research and the ability to respond to the social impacts of climate change.

Timeframe: Years 1–6 (2022–28)

Lead agency: MPI

Relevant portfolio: Agriculture

Primarily supports: Objective EF1

Status: Current

The Sustainable Food and Fibre (SFF) Futures Fund supports innovative projects that design and test new approaches and solutions to risks such as climate change in the primary sector. The fund supports innovation in Aotearoa New Zealand’s food and fibre sector by co-investing in initiatives that bring economic, environmental and social benefits for all New Zealanders. SFF Futures Fund projects include applied research that delivers tangible solutions for primary industries. Funding assists vulnerable groups, including rural farmers and Māori, with problem solving and innovation.

Timeframe: Years 1–6 (2022–28)

Lead agency: MBIE

Relevant portfolio: Research, Science and Innovation

Primarily supports: Objective EF1

Status: Current

These grants will boost investment in private sector research and development and support innovation. They will share the risk with Aotearoa companies. This means more climate-focused innovation should happen faster, to better enable adaptation action and the transition to a low-emissions economy.

Timeframe: Years 1–3 (2022–25)

Lead agency: MBIE

Relevant portfolio: Economic and Regional Development

Primarily supports: Objective EF1

Status: Current

This work will involve modelling the economic impacts of a changing climate on regional economies and providing guidance for assessing climate impacts in local economic decisions. This will help to identify likely impacts and determine where our vulnerable communities are by exploring the distribution of economic impacts across different parts of Aotearoa. These findings will help regions make informed risk assessments, actions and investments to reduce their exposure to climate-driven economic disruptions and support vulnerable communities. Regional economic preparedness will be further bolstered by other proposals in the national adaptation plan, such as the Māori-led partnership.

Timeframe: Years 1–2 (2022–24)

Lead agencies: Treasury; Toka Tū Ake EQC

Relevant portfolio: Toka Tū Ake EQC

Primarily supports: Objective EF2

Status: Current

Monitoring residential premiums and uptake of insurance gives a better understanding of the scale of shifts in insurance availability and affordability.

Timeframe: Years 1–6 (2022–28)

Lead agency: Treasury

Relevant portfolio: Finance

Primarily supports: Objective EF2

Status: Current

Treasury’s six-monthly economic updates are a core way to monitor and forecast the economic and fiscal environment. This includes the impact of shocks (eg, COVID-19 or natural disasters) on the Crown’s financial position and tracking long-run changes. The updates highlight known quantifiable and unquantifiable climate adaptation risks as a tool in fiscal and economic management.

“Adaptation is about surviving and thriving in the face of change.”*

Climate change is increasing the frequency and severity of drought in Aotearoa. From 2007 to 2017, drought cost the country around $720 million. The primary sector is particularly vulnerable and can expect conditions to get drier.

Climate disasters place a huge strain on the lives of farmers and growers, and particularly on their mental health. To reduce the economic risks of drought and build climate resilience in farmers and growers, a national long-term adaptation strategy is needed.

“Unless we work together, we are going to lock ourselves into the status quo.”

To develop a strategy that serves all stakeholders, a National Science Challenge consortium brought together farmers, growers, industry bodies, researchers and government. Online webinars and a one-day symposium were held in 2021. The resulting findings were captured in the Growing Kai Under Increasing Dry [PDF, 5.6 MB] report.

The report emphasises that it is vital for the primary sector to adapt and protect its viability, and to collaborate widely. Solutions include:

“We can be either proactive or reactive, but climate change impacts are inevitable.”

The report notes that although incremental adaptation has been happening for a decade, transformational change is now required. In contrast to incremental adaptation, which involves actions such as changing seed-sowing dates, transformational adaptation involves identifying novel land-use opportunities.

“Neither a top-down nor bottom-up approach alone will do.”

The report sets out key roles: farmers and growers are the decision makers on the ground; industry bodies work as knowledge brokers for adaptation; researchers contribute new possibilities for adaptation and co-develop solutions; and the Government has a significant role in enabling innovation, investment and flexibility.

* All quotes in this case study come from the National Science Challenge report, Growing Kai Under Increasing Dry [PDF, 5.6 MB]

Timeframe: Years 1–6 (2022–28) and ongoing

Lead agency: MPI

Relevant portfolio: Oceans and Fisheries

Primarily supports: Objective EF1

Status: Current

This report makes several recommendations for the fisheries management system and for commercial fishers. The Government’s response is underway and includes actions that support innovation across the system, progress an ecosystem approach to fisheries management and protect habitats of significance to fisheries management.

Timeframe: Years 1–6 (2022–28)

Lead agency: MPI

Relevant portfolio: Oceans and Fisheries

Primarily supports: Objective EF1

Status: Current

Building on scenario planning, the Seafood Sector Adaptation Strategy: Climate Adaptation Strategy 2021–2030 [The Aotearoa Circle website] is a collaboration between the major seafood sector leaders, Government, environmental non-government organisations, iwi representatives and the research community. The strategy sets out a shared 10-year vision and goals, and actions to help achieve these. The aim is to enhance the resilience and adaptive capacity of Aotearoa New Zealand’s seafood system. It includes actions to ensure adaptation information is more integrated and accessible, and to promote ecologically and economically efficient fishing and aquaculture. Te ao Māori is incorporated throughout the strategy – and specific implementation actions reflect this (eg, piloting and monitoring a te ao Māori approach to coastal management. An implementation group drawn from the strategy development agencies, established mid-2022, facilitates the strategy’s implementation and progress reporting.

“Only a collaborative, sector-wide adaptation strategy can address the impacts of climate-related risk in the seafood sector.”*

Climate risk to fisheries is one of the 43 risks identified in the National Climate Change Risk Assessment 2020. In 2020, the Aotearoa Circle brought together 23 organisations in the seafood sector to assess climate risks and opportunities. This was based on the Task Force on Climate-related Financial Disclosures framework.

This group included industry players, government, iwi and community stakeholders. It adopted the Seafood Sector Adaptation Strategy, with comprehensive actions to be brought in from 2021 to 2027.

“As kaitiaki we work together to adapt to climate change and ensure a resilient future.”

This is an early example of a sector working together with Government, iwi and stakeholders to produce an adaptation strategy, including an implementation roadmap. It is an opportunity to adapt in ways that bring lasting co-benefits to habitats, ecosystems, communities and businesses.

* All quotes in this case study come from the Aotearoa Circle Seafood Sector Adaptation Strategy: Climate Adaptation Strategy 2021–2030 [The Aotearoa Circle website]

Timeframe: Years 1–3 (2022–2025)

Lead agency: MBIE

Relevant portfolio: Tourism

Primarily supports: Objective EF1

Status: Current

The goal of this work is regenerative tourism. The first phase focuses on ‘better work’ and the second phase on the environment. The Tourism Adaptation Roadmap developed by the Aotearoa Circle will be an input for the environmental phase of the Tourism Industry Transformation Plan. This allows for a sector-wide assessment of risks and actions. Alongside action 10.15, this work will help to minimise the impacts of a changing climate on tourism workers, business owners and communities whose livelihoods depend on this at-risk sector.

Timeframe: Years 1–2 (2022–24)

Lead agency: MBIE

Relevant portfolio: Tourism

Primarily supports: Objective EF1

Status: Current

Currently, international visitors do not directly pay for many products and services they use where these are funded by local communities. The Ministry of Business, Innovation and Employment (MBIE), directed by the Minister of Tourism, is reviewing the International Visitor Conservation and Tourism Levy (IVL). This includes ensuring international visitors contribute to resilient, adaptable infrastructure and the natural environment they use during their visit. Resilient infrastructure, including a healthy environment, will reduce the risks from extreme weather. This action will support a focus on the spending priorities of the IVL, as well as any further work across the life of the national adaptation plan (eg, other tools) to support adaptation and climate resilience in tourism.

Timeframe: Year 1 (2022/23)

Lead agency: MBIE

Relevant portfolio: Economic and Regional Development

Primarily supports: Objective EF1

Status: Current

This action will check the current government’s procurement policy framework enables mitigation and adaptation in government investments. The greatest opportunity will likely be in construction contracts, making buildings and infrastructure resilient to a changing climate, and reducing carbon emissions and waste. This links to the Homes, buildings and places action plan (chapter 7).

Timeframe: Years 2–5 (2023–27)

Lead agencies: TPK; MBIE

Relevant portfolios: Māori Development; Economic and Regional Development

Primarily supports: Objective EF1

Status: Proposed

The aim of this work is to support Māori small and medium enterprises to develop low-emissions growth strategies, respond to climate-related risks and opportunities, and adopt resilient ways of working. Businesses would commit to reducing their emissions or improving their resilience to physical climate events.

This action will support Māori small businesses, which are disproportionately concentrated in sectors exposed to climate impacts and typically have less capacity to adapt than larger enterprises, to take action and demonstrate leadership in adaptation.

Timeframe: Years 1–6 (2022–28)

Lead agency: MBIE

Relevant portfolio: Small Business

Primarily supports: Objective EF1

Status: Proposed

This will help small businesses reduce their climate risks through targeted guidance and information. The guidance will be based on research that will increase understanding of what businesses are doing to adapt, and the pain points for business owners. The research will set a baseline for current action, inform future policy and drive the development of guidance and resources for small businesses.

This action will assist many of the businesses least able to adapt with climate adaptation, and least aware of the benefits of adaptation and effective ways to build resilience against climate risk. This will help ensure that the benefits of climate adaptation are distributed broadly throughout Aotearoa New Zealand’s business demographics.

Timeframe: Years 1–6 (2022–28)

Lead agency: MBIE

Relevant portfolio: Research, Science and Innovation

Primarily supports: Objective EF1

Status: Proposed

This action will pool knowledge and resources to solve sector problems. The partnerships will recognise the complexity and interrelatedness of issues, such as climate adaptation, and the need for sophisticated networks to test, scale up and spread innovation to help address challenges facing Aotearoa. These networks will speed up the connections and relationships needed to implement change at pace.

Aotearoa New Zealand’s economy is connected with all the other outcome areas in this plan. A number of other actions will also contribute to a resilient high-wage, low-emissions economy, notably:

Chapter 10 Economy and financial system

August 2022

© Ministry for the Environment