Sector policies and plans Ngā kaupapahere me ngā mahere o te rāngai

This section sets out policies and actions that will help reduce net emissions across different sectors.

| Energy | |

|---|---|

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

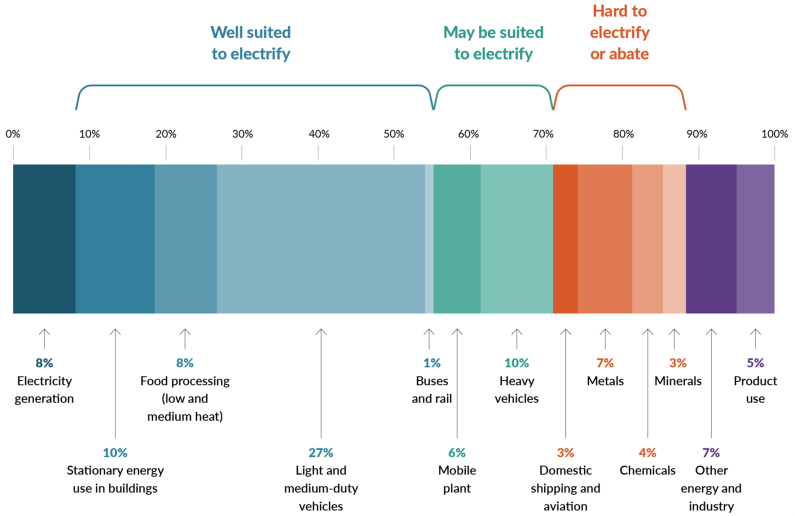

Emissions from energy use make up 37 per cent of New Zealand’s gross emissions. This includes 17.5 per cent from energy for transport. Figure 7.1 shows the makeup of emissions from energy, and industrial processes and product use. We expect energy emissions reductions in the second emissions budget (EB2) to come mainly from increased electrification and from energy efficiency gains in light transport and process heat.

It will take significant investment to meet expected demand for energy and achieve our goals. New Zealand needs investment in generation, transmission and local lines.

New Zealand’s energy sector is dominated by private companies. It is critical that we maintain investment confidence. Government intervention in the market can have an effect on investment. Therefore, we are taking an appropriate role by delivering policy and regulatory certainty, and a level playing field.

New Zealand does not subsidise renewables. Renewable energy already competes with fossil fuels, in part due to its abundance and because emissions pricing improves its competitiveness. Most of the known investment pipeline is renewable (largely solar and onshore wind, with some geothermal) and decarbonisation of the energy system will be guided by prices and markets. The Government’s role is to enable those markets to work effectively. The New Zealand Emissions Trading Scheme (NZ ETS) is central to reducing net emissions in the energy sector (see chapter 4).

New Zealand has faced recent challenges on energy security and affordability. The Government is committed to alleviating these problems. Tackling security and affordability concerns is a necessary precursor to giving businesses and households the confidence to electrify and reduce their emissions.

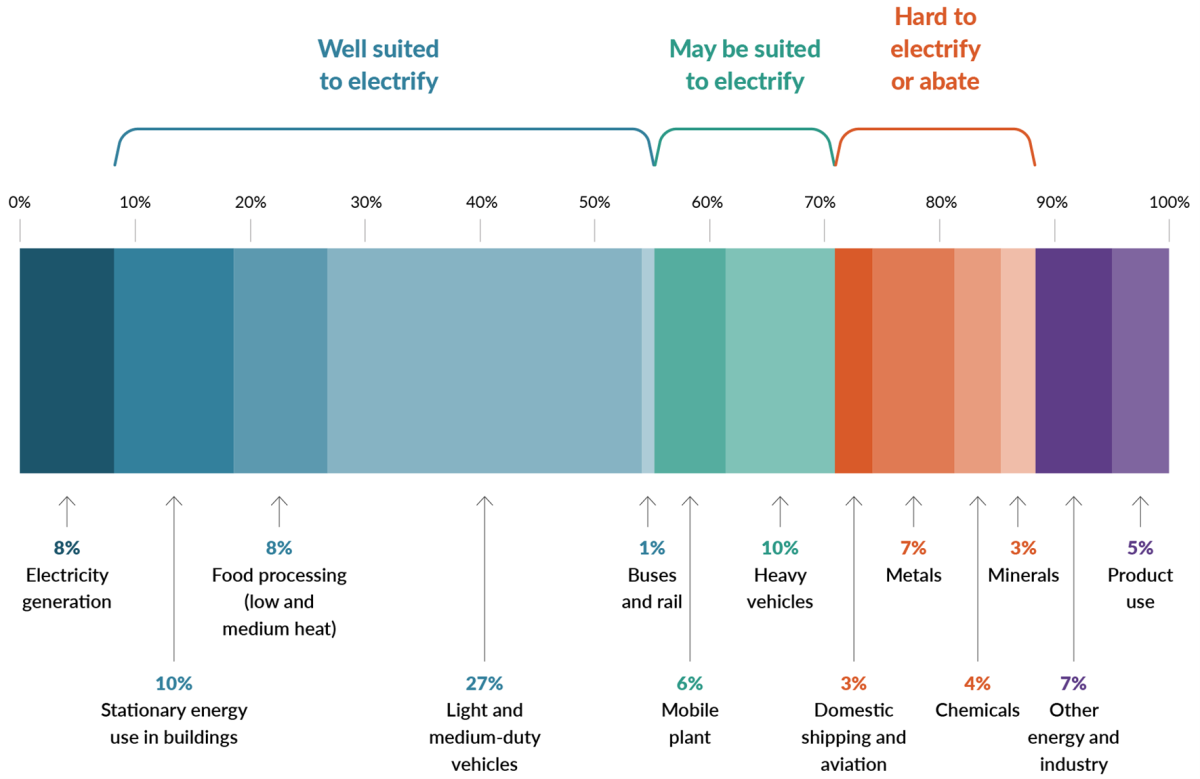

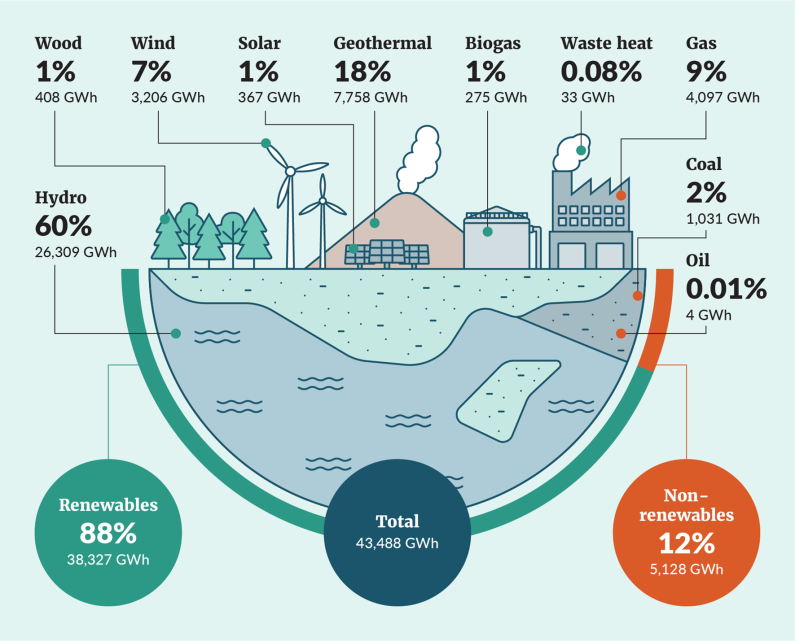

New Zealand has a high share of renewable energy (figure 7.2). Electricity demand is expected to rise significantly by 2050 as electric technologies are more widely adopted. This increase will outpace the demand growth of previous decades. Renewable generation capacity must be ready to meet this demand.

We need to enable new investments in electricity transmission and distribution infrastructure to improve the reliability of our grid. An estimated $100 billion of investment is needed by 2050 to build and maintain this infrastructure.5

5 Boston Consulting Group. 2022. The Future is Electric. Auckland: Boston Consulting Group.

The Government has committed to doubling renewable energy by 2050. Electrify NZ is the work programme to support private investment in electricity generation and networks that will enable us to achieve this goal.

Electrify NZ includes the following initiatives.

In 2023, gas contributed around 9 per cent of New Zealand’s electricity generation. Gas provides energy for industry, commerce and public use, and is a raw material in the production of methanol and urea. Gas-fired generation keeps electricity affordable and secure, which in turn supports electrification. Gas can also reduce our reliance on coal, which has twice the emissions impact.

We expect that as consumers switch to renewable energy, the demand for gas will reduce. However, we expect gas will continue to play a role in generation out to 2050. The electricity system currently relies on gas and a limited amount of coal to meet peak demand in winter and to cover dry years. Gas and coal are substitutes for each other for electricity generation. Insufficient gas supply could therefore result in New Zealand burning more coal to keep the lights on, increasing emissions.

The Energy Competition Taskforce brings together regulatory experts from the Commerce Commission and the Electricity Authority with observers from the Ministry of Business, Innovation and Employment. It will assess how well the market is delivering efficient investment and affordable electricity. The programme includes:

We are also working to minimise the impacts on those least able to pay. This includes continued support for the Warmer Kiwi Homes programme.

Work is underway to enable a smarter electricity system. This includes:

As we have seen in 2024, our energy security and affordability are under pressure. Work is underway to further improve the security of New Zealand’s electricity supply. This includes:

To address the current and longer-term risks to energy affordability and security, the Government is committed to a range of actions. These include:

The Government has also issued a Government Policy Statement to the Electricity Authority to:

In future, we may see more widespread adoption of technologies like hydrogen, sustainable aviation fuel and offshore renewable energy. Getting the enabling settings right now can support future emissions budgets.

The Government has agreed to create an enabling regime for carbon capture, utilisation and storage (CCUS). This will allow New Zealand’s industries to access CCUS technology on a level playing field with other reduction and removal tools.

The regime will include a financial incentive for CCUS operators through the NZ ETS. It will draw on international examples, which typically include assessment and monitoring, and a clear liability framework. Through 2025, the Government will progress legislation to establish the CCUS regime.

The most likely opportunity for CCUS is to establish sequestration facilities at existing gas fields during EB2 and third emissions budget periods.6 The regime will enable a gas operator to sequester carbon dioxide from their own production and from third parties. This will support the possible sequestration of carbon dioxide from our hard-to-abate industries, and from activities like direct air capture if and when they become economically viable.

6 This is additional to use of CCUS for geothermal generation, which is already happening.

We have taken steps to create an enabling environment and remove barriers to the uptake of renewable gases, including:

We are continuing to explore additional measures to increase the uptake of renewable gases. We will also review existing gas and related regulations, so they are fit for purpose and compatible with renewable gases in the reticulated system.

Diversifying fuels by replacing natural gas with low-emissions alternatives such as biomethane and hydrogen is a way to improve the security of our energy supply and reduce emissions.

There is an opportunity to use organic waste streams to capture biogas and upgrade it to biomethane. Biomethane is chemically identical to natural gas. It can be injected into gas transmission and distribution networks and used in existing appliances.

An estimated 4.9 petajoules of biogas (equivalent to about half of residential and commercial gas demand) is produced by landfills, wastewater treatment plants and industrial facilities every year. Much of this biogas is currently flared to reduce its global warming potential. Some of it is used on-site to generate electricity and process heat. There is also considerable potential for generation from agricultural waste sources.

Some biomethane supply is expected to come online for injection into gas distribution networks during the EB2 period. How much this will reduce New Zealand’s emissions depends on the wider energy system.

New Zealand has abundant bioenergy potential, stemming from its strong plantation forestry base. Bioenergy includes products such as woody biomass (chips, pellets) for use in boilers in industry and power generation, and liquid and gaseous forms such as renewable gases and sustainable aviation fuel. Enabling greater use of bioenergy increases the diversity of our low-emissions fuel, which in turn improves security of the supply.

Factors hindering uptake include price volatility, concerns about the security of supply over the life of an industrial plant (20-plus years), poor information on regional feedstock availability, and a lack of secondary processing at scale of bioenergy products (eg, into pellets).

We are supporting markets by providing information. The Energy Efficiency and Conservation Authority (EECA) is publishing insights to promote private sector investment in fuel-switching in the regions.

The Government will establish a domestic ministerial woody bioenergy taskforce to identify strategic opportunities for bioenergy. There is significant potential to make greater use of woody biomass for energy purposes to complement forestry resources for high-value economic activities. The taskforce will focus on investigating regulatory barriers to woody biomass uptake for bioenergy. More details on the taskforce will be released in 2025. See chapter 11 for more on the forestry sector’s role in the production of biomass.

Huntly Power Station, run by Genesis Energy, is New Zealand’s largest power station.

One of its roles is to provide back-up power when the country does not have enough renewable energy – for example, when the wind doesn’t blow, the sun doesn’t shine, or the rain doesn’t fall.

Three of the five generating units at Huntly can run on coal or natural gas. Coal generation from these units produced 1.35 Mt CO2-e of emissions from July 2023 to June 2024. Genesis Energy has a public goal of delivering 300,000 tonnes of biomass to Huntly Power Station by the end of fiscal year 2028. This fuel is intended to displace coal generation.

Initial government estimates suggest this could deliver reductions of 1.1 Mt CO2-e in the EB2 period and 1.6 Mt CO2-e in the EB3 period.

Image: Huntly Power Station

Geothermal generation makes up around 18 per cent of New Zealand’s total electricity generation and plays a vital role in decarbonising the electricity system and providing baseload generation.

Mercury is adding a fifth generating unit at Ngā Tamariki geothermal station, which will boost generation output by 46 megawatts at a cost of approximately $220 million. The station normally produces about 730 gigawatt hours of electricity each year, which is enough to power approximately 103,000 households. The expansion will increase this to 1,120 gigawatt hours per year or approximately 158,000 households once it is complete in 2025.

Mercury is also continuing to invest in technologies and processes designed to reinject non-condensable gases into the geothermal reservoirs. Releasing these gases is an inherent part of the geothermal generation process. Currently, around 98 per cent of Mercury’s Scope 1 emissions are attributed to fugitive emissions arising from geothermal generation.

Ngā Tamariki geothermal station has been successfully developing reinjection technology since 2022. The current reinjection rate is around 40 per cent of the station’s emissions. This translates to about 14,000 t CO2-e per year, equivalent to the emissions of about 1,800 households.7

Mercury is carrying out ongoing research and development to evaluate the effects of the current reinjection of non-condensable gases on the reservoir. It has begun trials to assess how to ensure continued sustainable management of the geothermal system. Over the next five years, it plans to expand reinjection to more geothermal sites.

7 Gen Less. Calculate your carbon footprint. Retrieved 23 November 2024. This calculation assumes 7.5 tonnes per household.

Image: Pipes at Ngā Tamariki geothermal station

New Zealand is a rich source of geothermal energy, which is used for electricity generation. Currently most geothermal wells are drilled to a maximum depth of around 3.5 kilometres, but it may be possible to access more energy if wells are drilled deeper.

Through the Regional Infrastructure Fund, the Government will invest in exploring the potential of supercritical geothermal technology (SCGT). SCGT could unlock more geothermal energy for New Zealand and further reduce reliance on fossil fuels in later budget periods.

Hydrogen is being trialled and demonstrated as a low-emissions alternative in heavy industry, heavy and specialty transport, production of green fuels (see below) and power generation.

Although hydrogen is not expected to play a significant role in EB2, it could in later budgets.

We aim to support private investment in hydrogen. The Hydrogen Action Plan focuses on:

Sustainable aviation fuels (SAF) support decarbonisation of air travel and the transportation of cargo.

The Government has funded feasibility studies with Air New Zealand to explore domestic supply chains of alternative jet fuel, including the use of woody biomass (forestry slash) and municipal waste. We intend to release the findings in 2025.

EECA and New Zealand Trade and Enterprise have also contributed funding for a feasibility study of producing SAF from green hydrogen at Marsden Point, by Fortescue Future Industries and Channel Infrastructure.

| Building and construction | |

|---|---|

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

Buildings contribute around 12 per cent of gross domestic greenhouse gas emissions. Building-related emissions come from the energy used to operate buildings (operational emissions, 9 per cent or 6.7 Mt CO2-e) and the emissions associated with the materials used to construct them (embodied emissions, just under 4 per cent or 2.8 Mt CO2-e).

About half (54 per cent) of operational emissions are from electricity, with the remaining 46 per cent from fossil fuels, mainly coal and gas.

Reducing emissions in the building and construction sector can support wider decarbonisation of the economy.

Energy-efficient buildings require less energy to run, creating fewer operational emissions and reducing the cost of running buildings, which encourages people to improve the energy efficiency of their buildings.

Our approach is to remove barriers and make information more accessible. This approach aims to enable households and businesses to make quicker, cheaper and easier decisions on lower-emissions materials and on the design and use of buildings. It can also help the market to function more effectively.

Currently, limited information on the energy performance of buildings is available for owners, buyers and renters.

Energy performance ratings provide verified and credible sustainability data to building owners and users. By enabling comparisons with other buildings, ratings can facilitate sustainable investments by revealing opportunities for building owners to improve energy efficiency at low cost.

Ratings also allow tenants to make informed choices when renting buildings. This can encourage landlords and developers to invest in energy efficiency.

New Zealand has a voluntary energy performance rating scheme called NABERSNZ. This scheme provides performance information about commercial office buildings and public hospitals. Some government agencies must obtain a NABERSNZ rating for office buildings they own or lease.

The Government intends to increase the availability of voluntary ratings by expanding the NABERSNZ scheme to other non-residential buildings such as shopping malls and hotels.

In Australia, NABERS ratings are available for 11 building types. Commercial office buildings over 1,000 square metres are required to have a NABERS rating. Rated buildings have reduced their energy use by over 40 per cent on average since 2010.8

8 NABERS. 2022. Energy efficiency in commercial buildings [PDF, 8.3 MB]. Retrieved 3 December 2024.

Around 70 per cent of the buildings that will exist in New Zealand in 2050 have already been built. Retrofitting buildings is therefore critical to reducing operational emissions.

We will investigate options to streamline compliance with building regulations to make it easier for people to voluntarily retrofit a building.

Embodied emissions can be reduced by:

The Government is already working on actions to support lower embodied emissions by:

Other Government actions include boosting domestic wood processing (chapter 11) and investing in resource recovery through the Waste Minimisation Fund (chapter 13).

New Zealand’s understanding of the embodied emissions of building materials has improved in recent years from a low base. However, limited availability of credible data and information can make understanding, comparing and reducing embodied emissions challenging.

Better and more accessible data can make it easier for consumers and building designers to understand and measure embodied emissions. This enables people to consider the emissions impact of design and construction choices.

The Government will work alongside the sector to encourage lower embodied emissions by:

These initiatives will help build strong evidence and improve the sector’s ability to make well‑informed decisions.

Auckland University of Technology’s (AUT’s) Tukutuku building accommodates around 2,200 students and staff within the Faculty of Health and Environmental Sciences. Tukutuku sets a new benchmark for sustainable tertiary education buildings in New Zealand while creating a vibrant, inclusive space for learning and collaboration.

Tukutuku’s careful design and orientation optimise natural light and indoor temperature and balance solar heat gains and losses. These design features have minimised the building’s energy use and operational emissions. Tukutuku also has extra insulation, a rainwater harvesting system and a displacement ventilation system. Together, these measures mean it is expected to be one of the most energy-efficient tertiary-education buildings.

Tukutuku is designed to use 60 kilowatt hours per square metre of energy annually. Operational emissions from running the building over 50 years are anticipated to be around 490 kilograms of CO2-e per square metre.

To minimise the embodied emissions associated with the construction materials, Tukutuku was built using an innovative, lightweight timber structure and repurposes parts of an existing building. The lightweight structure allowed the building to go up to four storeys whereas a heavier, more traditional system would have limited the height to three storeys because of the poor ground conditions. This construction approach resulted in Tukutuku creating only half the embodied emissions – around 448 kilograms CO2-e per square metre – compared with an equivalent industry standard building.

Further environmental and economic benefits were achieved by diverting over 90 per cent of the construction and demolition waste from landfill. This saved 40 per cent on disposal costs.

Image: Tukutuku building at Auckland University of Technology.

| Transport | |

|---|---|

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

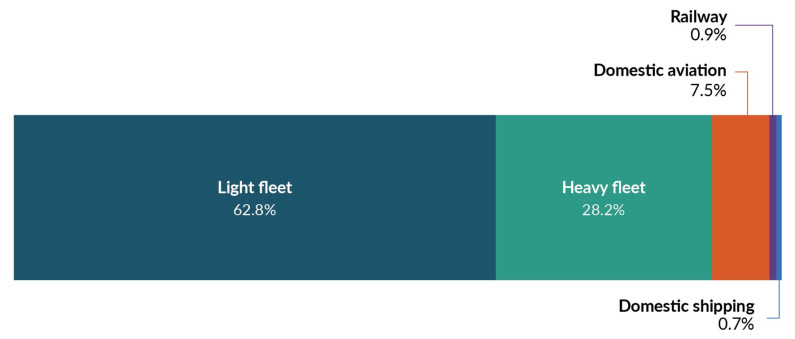

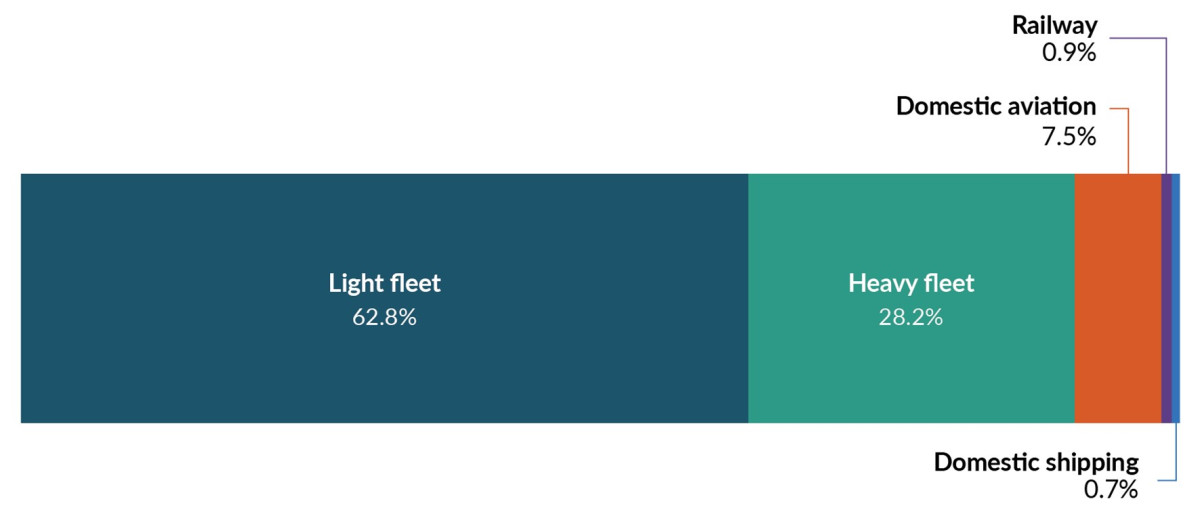

Transport was responsible for 17.5 per cent of New Zealand’s gross greenhouse gas emissions in 2022. More than 90 per cent of transport emissions are from road transport. New Zealand has the fifth highest per-capita transport emissions among developed countries. Transport emissions increased by 68 per cent from 1990 to 2022. This was mostly driven by population growth and economic activity.

Figure 9.1 shows the light vehicle fleet – typically cars and other vehicles for personal use – is responsible for 63 per cent of transport emissions. The heavy vehicle fleet – typically medium and heavy trucks – is responsible for 28 per cent.

The remaining 9 per cent comes from domestic aviation, rail, and domestic shipping and pipeline.

In general, the market for electric vehicles (EVs) is expected to make a big impact to transport emissions in the 2030s and 2040s. This will happen gradually as people and businesses replace their vehicles. By the end of November 2024, there were approximately 117,000 EVs in New Zealand, including plug-in hybrids, which is up 9.3 per cent from 1 January 2024.

‘Range anxiety’ and concerns about the availability of public charging points continue to hamper EV uptake. Accelerating the rollout of public charging points can address these concerns.

New Zealand currently has about 1,250 public charging points. Over 500 more are in development as of September 2024. This creates a good base network, including fast chargers every 75 kilometres along most of the state highway network.

However, New Zealand’s EV charging infrastructure is behind that of other countries. At the end of 2023, New Zealand had one public charging point for every 88 EVs. Most comparable countries have ratios of one charging point to fewer than 40 EVs.9

The Government has a target of a network of 10,000 public EV charging points by 2030. This is expected to meet all public charging needs. Some possibilities include:

9 The International Energy Agency’s annual Global EV Outlook for 2024 finds Australia has about one charging point to every 68 EVs, while the United Kingdom has one to every 31 and Germany has one to every 25. However, countries record charging-point numbers differently.

The Supercharging EV Infrastructure work programme sets out actions to facilitate private investment and review Government co-investment.

These actions include:

Although EV numbers are growing, the private sector may not provide charging infrastructure without demand. At the same time, demand for EVs may be restricted if there are not enough charging points.

The Government can solve this problem by co-investing in public charging points with the private sector.

Co-investment can also support specific sites that would not attract private investment but are important for an effective nationwide network. For example, tourism hotspots can see high peak demand but low demand for most of the year.

As the network scales up and regulatory barriers are removed, the private sector will likely be able to invest with more confidence.

It is timely to review the Government’s co-investment approach, so that it can reach its national network goal and maximise value. Until now, most public EV charging points have been set up with government co-funding from the Energy Efficiency and Conservation Authority.

The review will consider the scale of co-investment, how it is prioritised across charging point types and locations, the processes to apply for and receive co-investment, and how it could change as the market develops. Cost–benefit analysis will inform the design of an updated co‑investment model.

The Government is engaging with the EV charging market on this review. We expect decisions to be made in early 2025. This will support final decisions on changes to the approach, which will be implemented later in 2025.

Ngātea, a town in the Hauraki Plains, is an ideal location for an EV charging point as it sits at the heart of the ‘Golden Triangle’, a busy transport route between Auckland, Tauranga and Hamilton. However, the town’s existing electricity network does not have enough spare capacity to install high-speed EV charging points. Increasing the network’s capacity would have required difficult, time-intensive and expensive grid upgrades.

To solve this problem, Z Energy worked with PowerCo, the local electricity distribution business, and Kwetta, a New Zealand EV-charging solutions supplier. Its ‘Prime’ charging unit allows fast charging points to be installed without major upgrades to the grid. The Energy Efficiency and Conservation Authority saw the demonstration opportunity for the project and provided support through its Low Emissions Transport Fund.

Connecting directly to the high-voltage network, the Kwetta Prime unit combines multiple elements necessary for fast charging into a single module. This includes the high-voltage switch and transformer (usually installed by the local lines company) and the metering, distribution and conversion (usually installed by the customer). Charging is then provided by Kwetta’s Skyhook fast DC charging point.

This solution also uses static synchronous compensator technology, which helps manage voltage during charging to ensure the stability of the electricity supply. This greater stability, in turn, allows more power to be transferred and improves stability on the wider network.

The Kwetta charging point was commissioned in December 2023 at the Ngātea Z Energy station, after a short, three-month deployment phase. The Ngātea site can now support up to 500 kilowatts of fast charging, even during constrained periods.

This solution will enable charging point operators to install high-capacity EV charging in locations with constrained electricity networks.

Image: The Kwetta charging point at Z Energy in Ngātea.

The Clean Vehicle Standard (the Standard) came into effect on 1 January 2023. It aims to progressively reduce the average carbon dioxide emissions of light vehicles entering the fleet. It does this by setting annual carbon dioxide targets that vehicle suppliers must meet on average across the vehicles they import.

Signalling achievable targets well in advance helps compliance and minimises supply and price impacts for consumers. In 2024 the Government reviewed the Standard. The review concluded that the 2025–27 targets (apart from the 2025 target for passenger vehicles) were too stringent and, if unchanged, were unlikely to be achieved. The annual targets out to 2027 were subsequently eased to ensure that the Standard is effective, targets are achievable, and the Standard supports vehicle availability, affordability and choice for consumers. Additionally, targets were added for 2028 and 2029.

From January 2027, the Government plans to return to the practice of regular fuel excise duty (FED) and road user charges (RUC) increases. The Government Policy Statement on Land Transport 2024–2034 signalled an increase of 12 cents per litre to FED in January 2027 and a further 6 cents per litre in January 2028, followed by a 4 cents per litre annual increase starting in January 2029. The purpose of these changes is to support further investment in transport infrastructure.

Light EVs started paying RUCs in 2024, and currently may pay more than equivalent petrol vehicles (such as efficient hybrids) in FEDs. The Government will transition the entire light vehicle fleet to RUCs, and away from fuel tax, by 2027. This will ensure that all road users contribute to the upkeep of our roads, whatever vehicle they drive.

We will also introduce legislation to set up time-of-use schemes in New Zealand. This will improve traffic flows and shorten journey times by charging road users at certain times or locations, depending on how busy the roads are. The charge encourages some users to change their travel habits, so there are fewer people on the roads at the busiest times.

Time-of-use schemes will help lower emissions, increase productivity and enable New Zealanders and freight to get where they need to go quickly and safely.

Our freight is mainly carried on road by heavy trucks. Other heavy vehicles have key roles in other sectors such as waste removal and construction. Heavy vehicle emissions are currently about a quarter of our transport emissions.

Decarbonisation of heavy vehicles is at an earlier stage than light vehicles both globally and in New Zealand. Zero-emissions heavy vehicles (ZEHVs) make up less than 0.13 per cent of the national heavy truck fleet.

The freight sector and other commercial sectors using heavy vehicles are market-led and highly competitive. They are best placed to lead decarbonisation. The Government can support the sector to reduce heavy vehicle emissions by removing barriers. It will also protect access to overseas markets as other countries set increasingly stringent expectations about supply chain emissions.

Over the second emissions budget (EB2) period, we expect significant global improvements in heavy vehicles. This is likely to include better fuel efficiency in internal combustion engine (ICE) trucks, and the supply of more makes and models of ZEHVs. We expect the capital cost difference between ZEHVs and ICE trucks to keep reducing, and the range of ZEHVs to keep increasing as technology improves.

The current vehicle dimension and mass rules tend to favour trucks that are relatively heavy (for greater efficiency) but with relatively low axle weights (to reduce damage to roads and highways) compared with other markets. These rules affect a range of heavy vehicles, including some ZEHVs. For example, some battery electric trucks sacrifice payload for battery weight to meet the current rules, making them less competitive than ICE trucks. Hydrogen tanks on heavy vehicles can cause them to exceed volume constraints.

The additional weight of electric batteries may put these trucks in a higher driver licence category than the equivalent ICE model. This adds costs to businesses using these zero-emissions vehicles.

We will review the regulatory system for barriers to uptake of ZEHVs, including the impact of axle weights and licence categories. Any change must be balanced against the increased wear and tear on roads and bridges from heavier vehicles, as well as their higher maintenance costs.

We have launched the Low Emissions Heavy Vehicle Fund (LEHVF) to promote innovation and offset the cost of hundreds of heavy vehicles powered by clean technologies. Budget 2024 provided $27.75 million for the fund, which is administered by the EECA. This aims to help early adopters to overcome upfront cost barriers and accelerate the uptake of these vehicles – whether they are battery electric, hydrogen fuel cell or hybrid.

The EECA’s early high-level modelling estimates up to 500 diesel vehicles would be replaced by low- or zero-emissions vehicles by 2028 through the LEHVF. This scenario could reduce transport gross emissions by around 367 kt CO2-e over the EB2 and third emissions budget periods.10 There is uncertainty about which vehicles the market will choose, in terms of both size and technology type, which will affect actual reductions.

The Government will also consider the merits of extending the exemption of heavy electric vehicles from RUC, which is currently due to expire at the end of 2025.

10 The grant scheme estimates were modelled separately from other policies of the second emissions reduction plan, which used the Emissions in New Zealand model.

For the short term, we expect electric charging of heavy vehicles to occur mainly at private depots. Some of the barriers to charging will be addressed by actions on electricity network infrastructure and supply (chapter 7). We will continue to monitor the uptake of heavy electric vehicles, and whether there is any role for the Government to facilitate charging infrastructure for heavy vehicles.

Domestic aviation and coastal shipping emissions make up a small proportion of transport emissions (about 8 per cent). Sea freight and supply chains are key drivers of New Zealand’s economy. Playing our part in decarbonising these sectors helps us manage supply chain emissions to maintain access to international markets.

The Government’s role is to facilitate industry discussions through existing forums, consider regulatory barriers and ensure New Zealand’s interests are represented on the international stage. International cooperation will also prepare us to use new technologies as they become available.

The Government has established Sustainable Aviation Aotearoa, a group of private sector and government agencies supporting the decarbonisation of the aviation sector. The group is exploring ways to work with counterparts in other countries, such as Australia, on settings that would support sustainable aviation fuel supply and uptake.

During the 2+2 Climate and Finance Dialogue with Australia in July 2024,11 the Government committed to convening roundtables with the maritime sector. These will identify the conditions required for green routes between countries.

Bringing together diverse industry stakeholders, a pre-feasibility study was completed in 2023 for an Australia–New Zealand green shipping corridor.12 This could allow commercially operating ships to use alternative fuels.

Separately, Zespri13 partnered with the CMA CGM Group on a feasibility study for a green route from New Zealand to Europe.

Low- or zero-carbon shipping corridors could allow New Zealand to:

11 The dialogue is an annual meeting between the respective Ministers of Finance and Climate Change from New Zealand and Australia.

12 The study was completed by the Maersk Mc-Kinney Moller Centre for Zero Carbon Shipping.

13 Zespri International Limited is the largest marketer of kiwifruit globally. Its international headquarters are in Mount Maunganui.

Domestic coastal shipping is exposed to the NZ ETS price through fuel purchases. International shipping, including any international carrier of domestic cargo that is incidental to its international cargo, is excluded from the NZ ETS.

Annex VI of the International Convention for the Prevention of Pollution from Ships requires member countries to adopt measures to ensure that domestic voyaging ships operate consistently with the international requirements. New Zealand chose to apply the Annex VI international ship carbon-intensity requirements to coastal shipping. Other countries, such as Australia, use alternative measures.

The NZ ETS and the carbon intensity requirements are not direct duplicates. However, applying both regimes could disadvantage domestic coastal shipping against competing international operators that move freight around New Zealand and are not subject to the NZ ETS.

It is unclear whether engaging with the Annex VI requirements would support lower emissions from domestic coastal ships. We will review whether applying the Annex VI requirements is effective and should continue.

Reliable and accessible public transport enables more efficient use of New Zealand’s existing transport infrastructure – especially in the largest cities. It also supports our emissions goals.

We have proposed investments in several major projects in Auckland and the lower North Island, to be completed over the next decade. These include:

The Government is investing $802.9 million in the Wairarapa and Manawatū rail lines as part of a funding agreement with the NZ Transport Agency, KiwiRail, and the Greater Wellington and Horizons Regional Councils. This will deliver more reliable services for commuters in the lower North Island.

Realising the benefits of reliable and accessible public transport will require continued planning, delivery and maintenance to support growing populations and meet demand. Improvements will need to occur progressively through investments in and enhancements to infrastructure and services. This work includes:

Most public transport authorities have begun using zero-emissions buses in their public transport fleets, because of the economic, health and emissions benefits.

From 1 July 2025, authorities are required to procure only zero-emissions buses.

To support this transition, the Government has reconfirmed $44.721 million through Budget 2024 over four years. Co-funding will be available to authorities to:

| Agriculture | |

|---|---|

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

Agriculture is a critical contributor to the New Zealand economy and way of life, making up 82.9 per cent of goods exports and 12.4 per cent of overall employment.14

Export earnings from the primary sector were $60.4 billion for the year ending 30 June 2025, $3 billion higher than projected in December 2024. This momentum is expected to continue, with exports forecast to reach $63.2 billion in value by 2027.15

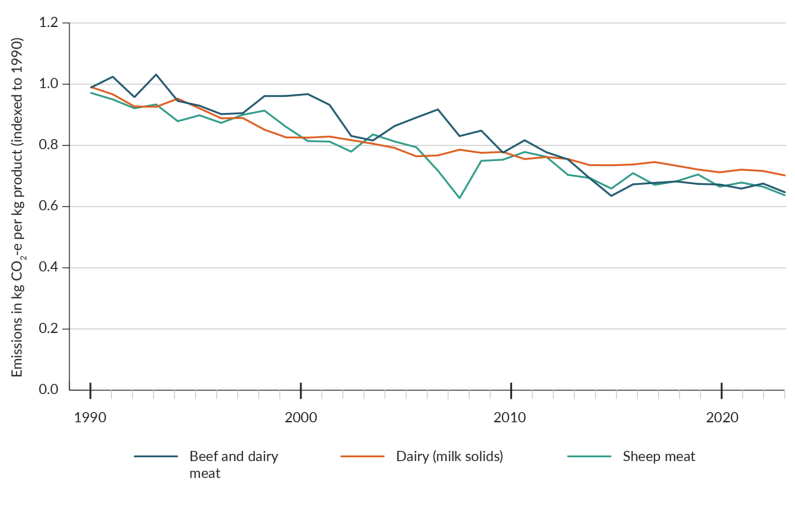

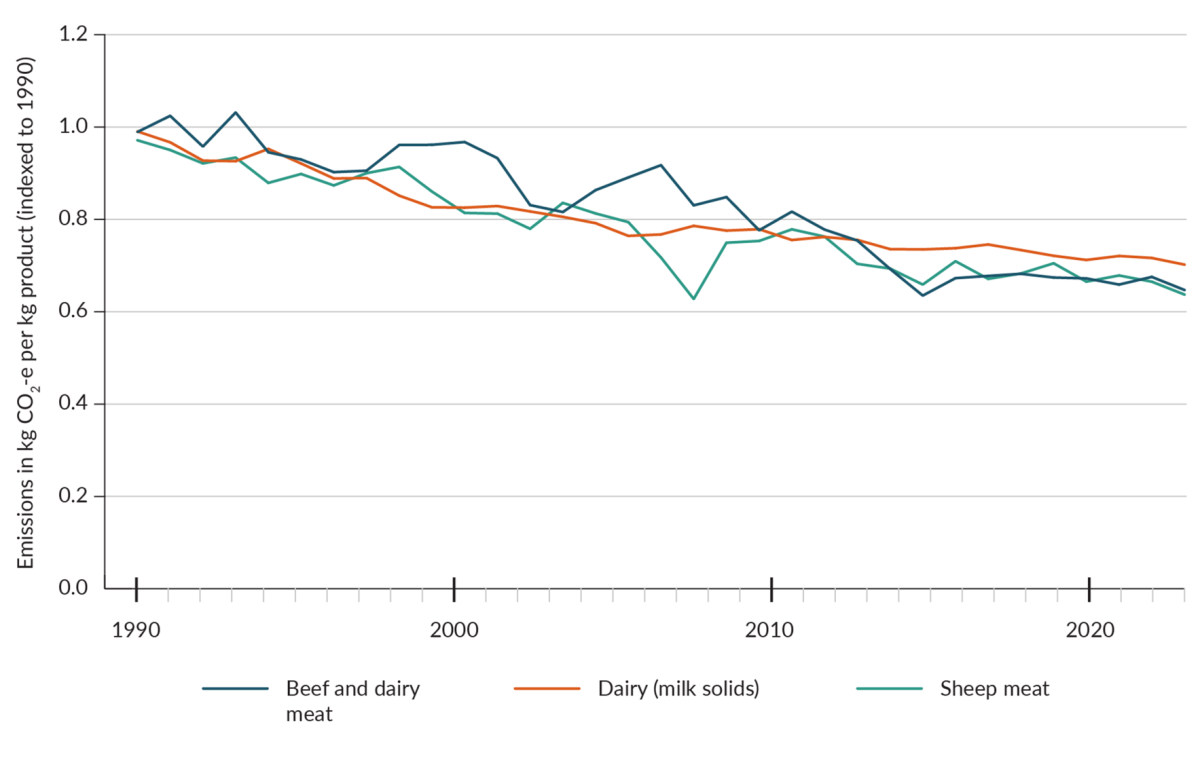

Agriculture also makes up over 50 per cent of New Zealand’s gross emissions. Importantly, New Zealand farmers are among the most climate-efficient producers in the world.16

We need to reduce agricultural emissions in a way that does not compromise exports or lead to emissions leakage. Climate change policies should not increase global emissions by shifting agricultural production to less efficient producers overseas. It is critical for the economy and for global emissions that New Zealand’s trade-exposed agricultural production remains competitive.

This is why the Government is taking a technology- and market-led approach to managing agricultural emissions, which we are making good progress in implementing.

Customers are increasingly demanding low-emissions products, which has knock-on effects through the supply chain. International and market-led action in response to this demand is increasing, and it is critical that the New Zealand agricultural sector keeps up. Taking action will help to maintain and enhance the competitiveness of New Zealand farmers and growers in markets demanding sustainably produced food, and the sector’s contributions to New Zealand’s economic prosperity.

Efficiency gains have been driven by farmer-led improvements in productivity, technology development and genetics improvements over time. These gains are expected to continue (figure 10.1).

We are seeing New Zealand agribusinesses setting ambitious, science-based targets to reduce emissions throughout their supply chains. We are also seeing increased demand from multinational companies looking to source their products from lower-emissions farms.17

Growing demand for lower‑emissions products may also create new financial opportunities to support on‑farm mitigation. Voluntary carbon markets (VCMs) have the potential to fund and reward the uptake of mitigation activities and technologies. Work underway, such as on the sustainable finance taxonomy, can unlock more investment and greater confidence in VCMs. For more information on the VCM work programme, see chapter 5.

14 Ministry for Primary Industries. 2025. Situation and Outlook of Primary Industries December 2025. Retrieved 6 January 2026.

15 Ministry for Primary Industries. 2025. Situation and Outlook of Primary Industries December 2025. Retrieved 6 January 2026.

16 For example, see: Mazzetto AM, Falconer S, Ledgard S. 2022. Mapping the carbon footprint of milk production from cattle: a systematic review. Journal of Dairy Science 105(12): 9713–25; Mazzetto AM, Falconer S, Ledgard S. 2023. Carbon footprint of New Zealand beef and sheep meat exported to different markets. Environmental Impact Assessment Review 98, 106946.

17 New Zealand food and fibre producers face a range of company initiatives, including:

Compared with the primary sectors in other developed countries, agriculture contributes a relatively high proportion of New Zealand’s emissions. It also makes up a more significant portion of gross domestic product.

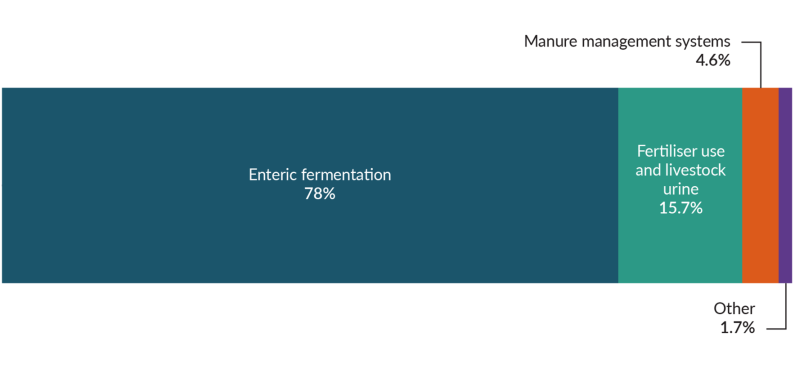

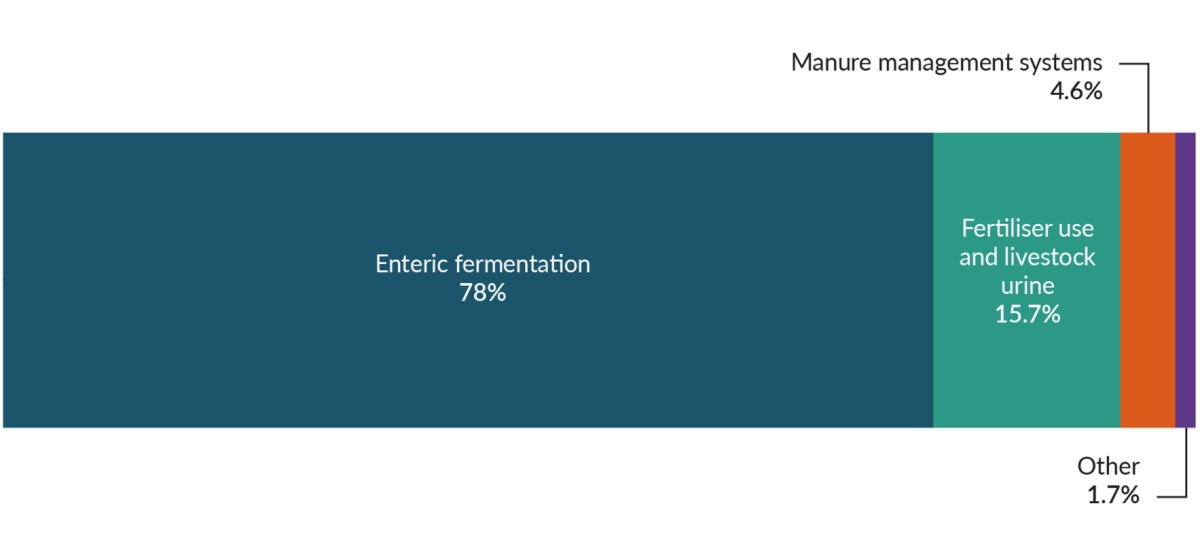

Figure 10.2 shows agricultural emissions by activity. Of the total of these emissions:

Of the 2023 agricultural emissions, the most significant come from dairy cattle (48.3 per cent), sheep (22.9 per cent) and beef cattle (20.1 per cent). Most emissions from agriculture are methane. Methane is a short-lived gas compared with other greenhouse gases, but it has a much greater warming effect.18

18 New Zealand has taken a split-gas approach to emissions reduction to recognise the distinct warming impacts of different gases. The split-gas approach recognises that biogenic methane (from agriculture and waste) is a ‘short-lived’ gas with a shorter atmospheric lifetime and a different warming impact, compared with other long-lived greenhouse gases, such as carbon dioxide. Long-lived gases can persist in the atmosphere for centuries, contributing to long-term warming. Future emissions of long-lived gases will add to the warming caused already until those emissions are reduced to net zero (previously emitted gases will continue). Biogenic methane, as a short-lived gas, does not have to reduce to zero emissions to limit global warming.

We remain committed to taking a multi-pronged approach to reducing agricultural emissions without undermining profitability. This approach involves:

Since the second emissions reduction plan (ERP2) was released, the Government has revised its approach to reducing agricultural emissions. In particular, we will no longer be introducing an on-farm emissions pricing system by 2030. Reducing biogenic methane emissions without introducing agricultural emissions pricing is feasible – and is an outcome the agriculture sector is already making progress towards.

The Government has committed more than $400 million over four years to accelerate the development and commercialisation of tools and technologies to reduce emissions, including through the Ag Emissions Centre and AgriZeroNZ. This investment is:

This investment programme is critical to growing the technology pipeline.

AgEC was established in 2009 as the New Zealand Agricultural Greenhouse Gas Research Centre. It funds a world-leading science programme that drives excellence in the research and development of innovative tools and technologies to reduce agricultural emissions.

AgEC engages scientists to deliver cutting-edge research on emissions mitigation that supports New Zealand farmers and strengthens our pasture-based competitive advantage – fuelling the innovation pipeline. Its investment, which industry and other cofunding supplements in many areas, is foundational to support the pipeline of products for commercialisation, and also benefits farming resilience. The funding portfolio includes:

AgEC also supports communications and training by providing clear, science-based information. This includes explaining how mitigation works, demonstrating progress on new tools and technologies, and helping farmers to make informed decisions about adopting these solutions.

Supporting the availability of and access to greenhouse gas measurement infrastructure is a critical enabler of R&D progress. AgEC monitors the supply and demand of infrastructure required for measuring greenhouse gas emissions and has supported several infrastructure upgrades. Examples of this work include supporting the expansion of testing and measurement facilities at Pāmu and the New Zealand Ruminant Methane Measurement Centre. AgEC also leases C-Lock GreenFeed19 units to research organisations for shed- and field-based methane measurement.

Established in 2023, AgriZeroNZ is a public–private partnership. One half is owned by the Crown and the other half by leading agribusinesses and banks: Fonterra, Ravensdown, Silver Fern Farms, Synlait, The a2 Milk Company, ANZCO Foods, Rabobank, ANZ Bank, BNZ Bank and ASB Bank. The AgriZeroNZ limited partners have agreed that AgriZeroNZ, as the Government’s primary vehicle for supporting commercialisation of agricultural greenhouse gas mitigation tools, will take a stronger role in supporting the adoption of new mitigation technologies.

AgriZeroNZ is actively exploring opportunities to accelerate farmer uptake and de-risk initial tool rollout. Through targeted investment and actions, AgriZeroNZ is accelerating the development, commercialisation and/or deployment of effective and affordable solutions that New Zealand farmers and others will use to significantly reduce emissions.

Industry and the Government have committed $191 million to AgriZeroNZ over its first four years. This funding is to support the partnership’s ambition to ensure all farmers in New Zealand have equitable access to affordable, effective solutions that reduce biogenic methane and nitrous oxide emissions. Key goals are to support a 30 per cent reduction by 2030 and enable the development and adoption of solutions that drive emissions towards ‘near zero’ by 2040.

As at 30 September 2025, AgriZeroNZ has committed $71.1 million across 16 companies and projects in areas such as a methane-inhibiting bolus, vaccines and inhibitors, probiotics and natural enzymes, pastures, cow-wearable technology and genetics solutions. AgriZeroNZ is also supporting the adoption of greenhouse gas mitigation tools by New Zealand farmers.

Through the GRA, the Government is partnering with other countries in research related to New Zealand’s interests (eg, the Ireland–New Zealand Joint Research Initiative). The GRA enhances New Zealand’s domestic research capacity and connects the country’s scientists with key partners.

Over 140 New Zealand scientists have collaborated on more than 70 large multinational research programmes. Global collaboration has generated new insights into areas of particular relevance to New Zealand. For example, research on the biology of the rumen led to the current research on methane inhibitors and vaccines, the impact of feeds and genetics, and management practices.

The GRA also supports developing countries to build capability to contribute to reducing global agricultural emissions. It promotes understanding of the challenges involved in addressing greenhouse gases while maintaining and increasing food production. New Zealand has partnered with 15 developing countries to help improve their greenhouse gas inventories and in this way support their understanding of their own emissions. These countries are improving their emissions accounting to meet the same standards as New Zealand works to.

19 A technology designed to measure greenhouse gas emissions from livestock.

The R&D pipeline has a growing number of very promising mitigation tools that collectively have a high abatement potential.20

New Zealand’s farming and growing systems are diverse, and not all mitigation tools will work for all systems. This is why the R&D programme focuses on delivering a range of adoptable solutions, across different system types. We expect that tools developed in New Zealand will be able to be exported and used internationally – bringing further potential benefit.

We are investing in a portfolio of high-impact emissions reduction technologies suitable for a range of pasture-based farming systems, including long-lasting inhibitors and probiotics, genetics, pasture and manure management activities. This range will give farmers choices and means that successful mitigation will not rely on a single technology.

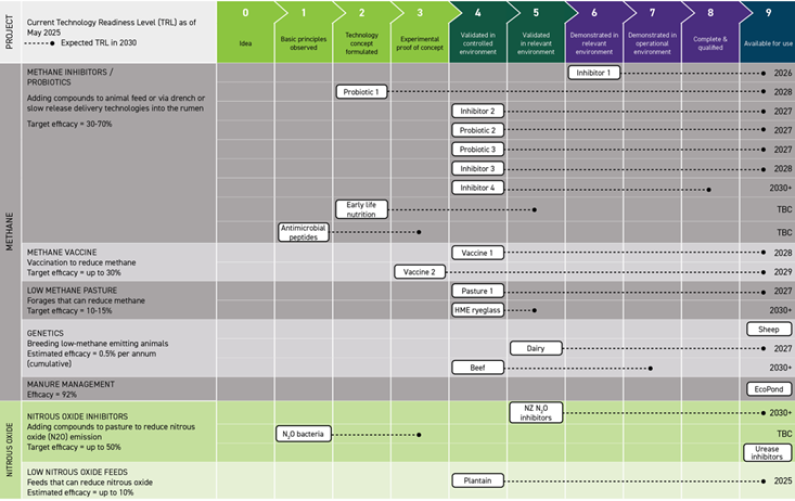

Figure 10.3 shows a range of tools21 that have been invested in across key sectors in New Zealand. It also lists estimates of efficacy and commercial availability. These estimates are a snapshot in time, subject to varying uncertainty, and estimates will change as technology develops and progress is made through the regulatory system.

We expect to see the uptake of mitigation solutions increase over time, including to support meeting market-driven supply-chain targets and our own climate change targets.

Since ERP2 was published in December 2024, the range of mitigation options available in the market has expanded and a wide range of solutions in development has progressed. For example:

20 As more mitigation tools emerge, we will also need to understand their ‘stackability’ – that is, what happens to emissions when multiple tools are used at the same time. In our modelling, we assume no additionality between tools that target the same source of emissions. This assumption is conservative in that some interventions might ‘stack’, but we cannot count on them doing so at this stage as this effect needs to be demonstrated through research.

21 Many other mitigation tools currently in development in other countries might also come to New Zealand.

This figure indicates estimates as at May 2025. In most cases, companies developing the tools have provided these estimates. The dates and details are subject to change as projects progress through the pipeline and noting these are early-stage technologies. Ongoing scanning of new technologies and research is also occurring. This diagram does not include work underway on soil carbon and farm systems management, and other supporting research. Some technologies will be stackable, while others will not be as they have similar modes of action.

Note: * The earliest possible year for market availability is shown. The actual year depends on regulatory and approval timeframes and pricing structures.

TBC = To be confirmed. The project is in an early stage so it is not possible to predict when it will be available yet.

New Zealand-based Ruminant BioTech has developed world-leading methane inhibitor technology, with its long-duration bolus platform capable of reducing daily methane emissions in cattle by over 70 per cent for up to 100 days. The bolus platform will be the first commercially viable methane mitigation product for extensive beef producers in New Zealand, providing a simple, practical and highly effective solution specifically designed for grass-fed pastoral farming operations.

Over recent years, the company’s R&D programme has focused on finetuning this technology, including through extensive testing to ensure it is safe for animals and has no adverse impact on the quality or safety of the food produced.

New Zealand farmers have used boluses for over 50 years, most commonly to deliver medicines and trace elements or minerals. Administered to the animal by mouth with an applicator specially designed for the purpose, the bolus moves through the digestive tract to establish itself in the animal’s rumen. Once in place, the bolus releases an optimal dose of active ingredient over a prolonged period to suit our pasture-based farming system.

To date, the company has concentrated on delivering a bolus for non-lactating cattle weighing between 350 and 450 kilograms, with plans to further develop this solution to all beef and dairy cattle. Broad adoption of the bolus platform will ensure New Zealand has a significant impact on reducing greenhouse gas emissions from the agriculture sector to meet its 2030 emissions reduction targets.

Image: Methane inhibitor technology for dairy cattle.

Users and markets must be assured that products are safe and effective. The Government wants regulation that is fit for purpose.

The Government is progressing work on the Agricultural Compounds and Veterinary Medicines Act 1997 (ACVM Act) and Hazardous Substances and New Organisms Act 1996 (HSNO Act) to:

The Ministry for Regulation reviewed the ACVM Act and HSNO Act to improve access to new agricultural and horticultural products. The Ministry for Regulation provided its recommendations to Cabinet in early 2025, and the Ministry for Primary Industries and the Ministry for the Environment are developing an Omnibus Bill that amends both the ACVM and HSNO Acts to address a number of these recommendations. It is anticipated that the Omnibus Bill will be introduced to the House in early 2026.

To fulfil its commitment to open access to gene technologies, the Government is progressing the Gene Technology Bill. The Bill seeks to enable greater use of gene technology, while supporting strong protections for the health and safety of people and the environment.

As New Zealand’s food and fibre sector makes up 82.9 per cent22 of our goods exports, it is critical that markets accept our produce when a new mitigation technology has been used to reduce emissions in animals or crops. This is why the Government has a programme to proactively support market acceptance. An example is New Zealand’s work to support the development of a Codex23 food safety standard for inhibitors in animal products, with the aim of encouraging the uptake of these technologies and facilitating trade.

The Government is also working to support recognition of the use of emissions reduction tools in the New Zealand Greenhouse Gas Inventory, so that efforts on-farm contribute to our targets.

22 Ministry for Primary Industries. 2025. Situation and Outlook of Primary Industries December 2025. Retrieved 6 January 2026.

23 International food safety standards are set by the Codex Alimentarius Commission, in which New Zealand is an active participant.

Currently, farmers have a range of ways to estimate emissions, but many of these measures differ in the results they give. For farmers, standardisation will provide a consistent foundation to inform their investment in new technology. For processors, it will increase confidence in their greenhouse gas reporting.

There are three components to the action ‘Developing measurement of on-farm emissions for use by 2025’.

This action is now complete, and the Ministry for Primary Industries is continuing work to enhance its methodology and tools. New mitigation technologies will be incorporated in the calculations as they emerge.

To reduce emissions, producers may need advice on adopting approaches that best fit their farming system.

Government support builds on the existing public and private advisory services sector. An example is the Ministry for Primary Industries’ On Farm Support programme, which has 53 regionally based staff who provide on-the-ground assistance to farmers, growers and catchment groups. On Farm Support helps them build on sustainability practices and navigate climate, water and environmental requirements, supported by integrated farm planning. It can connect farmers and growers to resources, advice, funding opportunities and extension services − offered by the public and private sectors, and industry organisations.

We expect extension services to support other policies across the second and third emissions budgets. Their effect on emissions is included in the reductions projected to occur through uptake of technology.

Māori farmers face a unique set of challenges in reducing agricultural emissions. As New Zealand works to lower emissions, collaboration between the Government and Māori is needed to address risks and realise opportunities for the Māori economy.

The Ministry for Primary Industries partners with Māori land owners and agribusinesses to codesign solutions that align with Māori values and can scale within and beyond their catchment communities. This work includes:

For more detail on the specific impacts of climate policies on Māori and how these impacts can be mitigated in partnership with Māori, see chapter 14 and chapter 15.

In 2024, the Government appointed an independent panel (the panel) to review New Zealand’s biogenic methane science and 2050 target. The panel provided an up-to-date assessment of methane’s warming impact, and advice on a biogenic methane target consistent with the principle of no additional warming for New Zealand. The Government considered advice from the panel, the Climate Change Commission | He Pou a Rangi 2050 target review and officials, weighing the scientific findings alongside the economic and climate objectives to determine the new target to put to Parliament.

In December 2025, Parliament amended the Climate Change Response Act 2002 to reflect a new biogenic methane target of 14 to 24 per cent below 2017 emissions by 2050. The new target provides farmers and exporters with a clear pathway to reduce emissions while maintaining productivity.

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

Forestry is the only form of carbon removal currently recognised as contributing to New Zealand’s domestic and international climate targets. Forests can be either a carbon sink (while growing and when turned into long-lived wood products such as building materials) or a source of emissions (eg, through deforestation).

The Ministry for Primary Industries’ September 2024 baseline projections indicate the land use, land-use change and forestry sector is projected to remove between 52.7 and 62.6 Mt CO2-e from the atmosphere in the second emissions budget (EB2) period (table 11.1). The projections have been updated since consultation to align with the accounting methodology for reporting on emissions reduction.

The lower scenario has been revised in response to consultation feedback.19 This is based on the 2023 afforestation intentions survey findings, but limits exotic afforestation to the lower range of estimates.

19 The lower scenario results are revised from the ERP2 discussion document. They result in about 29,000 fewer hectares of exotic afforestation over 2024–26, and removals reduced by about 0.3 and 1.9 Mt CO2-e for the lower scenario during the EB2 and EB3 respectively.

| Scenario | EB1 (2022-25) | EB2 (2026-30) | EB3 (2031-35) | 2050 |

|---|---|---|---|---|

| Lower | -21.0 | -52.7 | -66.3 | -15.1 |

| Central | -25.2 | -60.7 | -82.0 | -21.8 |

| Upper | -26.6 | 62.6 | -86.7 | -27.9 |

20 Target accounting emissions include gross emissions, along with a subset of forestry and land-use emissions and removals. Target accounting is designed to be compatible with net emissions targets, under which business-as-usual removals from pre-1990 forests are not counted. Only emissions and removals due to additional human activities are counted. This means emissions from deforestation are counted for all forests, but to address permanence, removals from afforestation are only counted for post-1989 forests up until their long-term average is reached.

Projected exotic afforestation will be an important contributor to the budgets. However, newly planted forests take time to start sequestering carbon. They also create emissions from clearing land and soil. As a result, new exotic afforestation in the EB2 period will start contributing carbon removals in later budgets.

Carbon removals from many exotic production forests that were planted in the early 1990s are slowing as the forests reach maturity and harvest. However, these existing forests will contribute more to the first emissions budget (EB1) and EB2 than any new planting that occurs (or has already occurred) in these periods.

Forestry and wood-processing policies that support the displacement of emissions from other sectors contribute to reducing emissions (eg, wood products replacing higher-emissions products). However, these impacts can be hard to model because of differences in underlying assumptions, high uncertainty and the potential for double counting.

Forestry removes carbon dioxide from the atmosphere, reducing net emissions. Wood processing can reduce gross emissions by producing high-value products to replace emissions-intensive ones such as steel and concrete.

The Government’s strategy is to restore confidence and certainty in the forestry and wood-processing sector. This will unlock its full potential to help rebuild the economy, expand exports and meet our climate targets, while balancing productive land uses between forestry and agriculture.

The policies and initiatives included in this plan are part of a wider government programme and will further build confidence by getting the incentives right for forestry and improving the investment environment for high-value wood processing.

Over the last few years, we have seen greater investment in forestry, particularly exotic forestry, due to the significant increase in the New Zealand Emissions Trading Scheme (NZ ETS) price. The increased planting will help us meet emissions budgets cost-effectively through the carbon stored as the forests grow. It supports other forestry objectives – for example, for sustainable land management and increased fibre supply.

It is important to balance productive land use between forestry and agriculture. If left unchecked, increases in farm conversions to forestry on high-quality land can affect those with interests in these sectors, local communities and food production. Appropriate incentives, including restoring price stability and confidence in the NZ ETS (chapter 4), will balance encouraging afforestation for increased carbon sequestration with other land uses. The following policies aim to achieve this.

The Government is taking action to protect productive farmland and support sustainable forestry growth. At current (and higher) NZ ETS prices, exotic forests are cost-competitive with pastoral land uses, driving whole-farm conversions to forests. While these forests can help us meet our climate targets, they can also have undesirable impacts on rural communities, agricultural supply chains, local employment, economic activity and land-use flexibility.

We are fixing this by limiting the number of NZ ETS registrations for whole-farm conversions to exotic forestry on high-quality productive land. This policy aims to balance productive land uses to ensure the best use of land for New Zealand in the long term and retain farmers’ flexibility.

Although the proposals will involve some change to current NZ ETS settings, the aim is to provide greater certainty in the NZ ETS in the medium term through clear rules to support forestry investment and emissions reductions.

The Government is exploring opportunities to partner with the private sector to plant trees on Crown-owned land (excluding national parks) that is of low conservation value and low farming value. These public-private partnerships could help New Zealand meet climate change targets and create more jobs in the forestry and wood processing sector.

There are opportunities to plant both exotic and native trees on Crown-owned land. Exotic forestry sequesters carbon more quickly and offers a way to use land more productively where suitable for plantation forestry. Native forests grow more slowly, but can provide longer-term carbon sinks and co-benefits, including biodiversity and adaptation.

The Government will release a request for information in late December which will help clarify the circumstances and conditions under which potential partners are interested in taking forward opportunities to plant on Crown-owned land. This will help the Government understand what land may be suitable to offer for partnership. Proposed afforestation on Crown-owned land will not contribute to achievement of EB2, but can contribute to reaching net zero for all greenhouse gas emissions, except biogenic methane, by 2050. The technical annex provides further details of the impact of this policy on sufficiency.

Boosting wood processing will result in more long-lived wood products, which store carbon during their lifetime. It will also grow the economy, provide regional jobs and create export potential. There are significant opportunities for growth in these products. For example, modern engineered timber in construction could replace emissions-intensive materials such as steel and concrete, while also storing carbon. We expect that wood solutions will become more mainstream, and their costs will continue to fall.

The low-grade logs we currently export could be used to produce high-value wood products, including:

We are also investigating providing NZ ETS credits for wood processors based on the embedded carbon captured in longer-life timber products.

Chapter 8 includes actions to improve access to information for choosing sustainable building products.

Woody biomass can comprise any woody material from a forest, including material left after harvest, residues from wood processing (ie, sawdust and woodchips) and logs from plantings of fast-growing trees (ie, pulp forest or biomass crops). Woody biomass can be used as a feedstock to produce low-emissions fuel substitutes such as wood pellets. These produce high temperature heat for industry and sustainable aviation fuel.

We are progressing a biomass planting programme (5,000 hectares of plantation forest is planned) to increase the supply of biomass in targeted regions and to give insights for private investment in supply-side infrastructure. Research underway will also improve guidance on growing and harvesting woody biomass. In the future, we can expect more industrial process heat to be fuelled by woody biomass.

The Government is improving the resource consenting framework for wood processing to make it easier to establish new facilities and to re-consent existing ones. This will give wood processors longer-term certainty to invest in production and innovation. We have begun to improve consenting for infrastructure and other activities that will support forestry and other primary production, including through the fast-track regime discussed in chapter 7.

For wood-processing facilities, we are proposing to mandate a maximum processing time of one year for consents of both new and existing wood-processing facilities. We are also considering options to streamline re-consenting of existing facilities. This work will be progressed as part of the Resource Management Act 1991 reform.

Set up in 2003, the Wood Processing Growth Fund (WPGF) helps wood processors increase New Zealand’s onshore capacity. By boosting domestic wood processing, the WPGF will support the sector to store more carbon in long-lived wood products.

The fund seeks to unlock private capital through investment support to overcome the barriers facing the industry. In its first year, the WPGF has made investments that are:

Forestry has several environmental co-benefits, including erosion control (eg, intercepting rain, reducing run-off and sedimentation, and anchoring erosion-prone soils). These will become increasingly important for adaptation as severe weather events rise in frequency. More information on adaptation is in chapter 16.

Forestry can also have negative impacts if not managed well. These impacts include risks to water quality and biodiversity, and a greater risk of wildfires and wilding conifers. Increasingly severe weather events can mobilise slash and other woody debris from forests to damage downstream infrastructure, property and low-lying areas.

We understand the need for environmental policies and regulations to help manage the risk of negative impacts.

The National Environmental Standards for Commercial Forestry (NES-CF) are the main regulatory instrument for managing the environmental impacts of commercial forestry. They provide nationally consistent standards for managing eight of the main activities carried out by commercial forests, including afforestation, harvesting and replanting.

The NES-CF is part of the broader resource management framework, which is currently being reformed. The reform includes a review of slash management regulations in the NES-CF to ensure they are evidence-based and fit for purpose. Amendments will enable foresters and councils to focus on the most at-risk areas in order to prevent mobilisation that harms freshwater environments and downstream communities.

As part of changes to the Resource Management Act 1991, we are strengthening the penalties regime, with the guiding principle that low-risk activity should be permitted. However, penalties exist for people who break the rules. This includes any offences in forest harvesting, such as failure to comply with slash management regulations.

The Government is also developing national direction for natural hazards. This could cover other environmental risks linked to forests, such as landslips, erosion and wildfire. This work is expected to cover commercial forests and to direct councils on how to identify natural hazards, assess the risks and respond through their planning and consenting.

Chapter at a glance

Non-forestry removals |

|

|---|---|

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

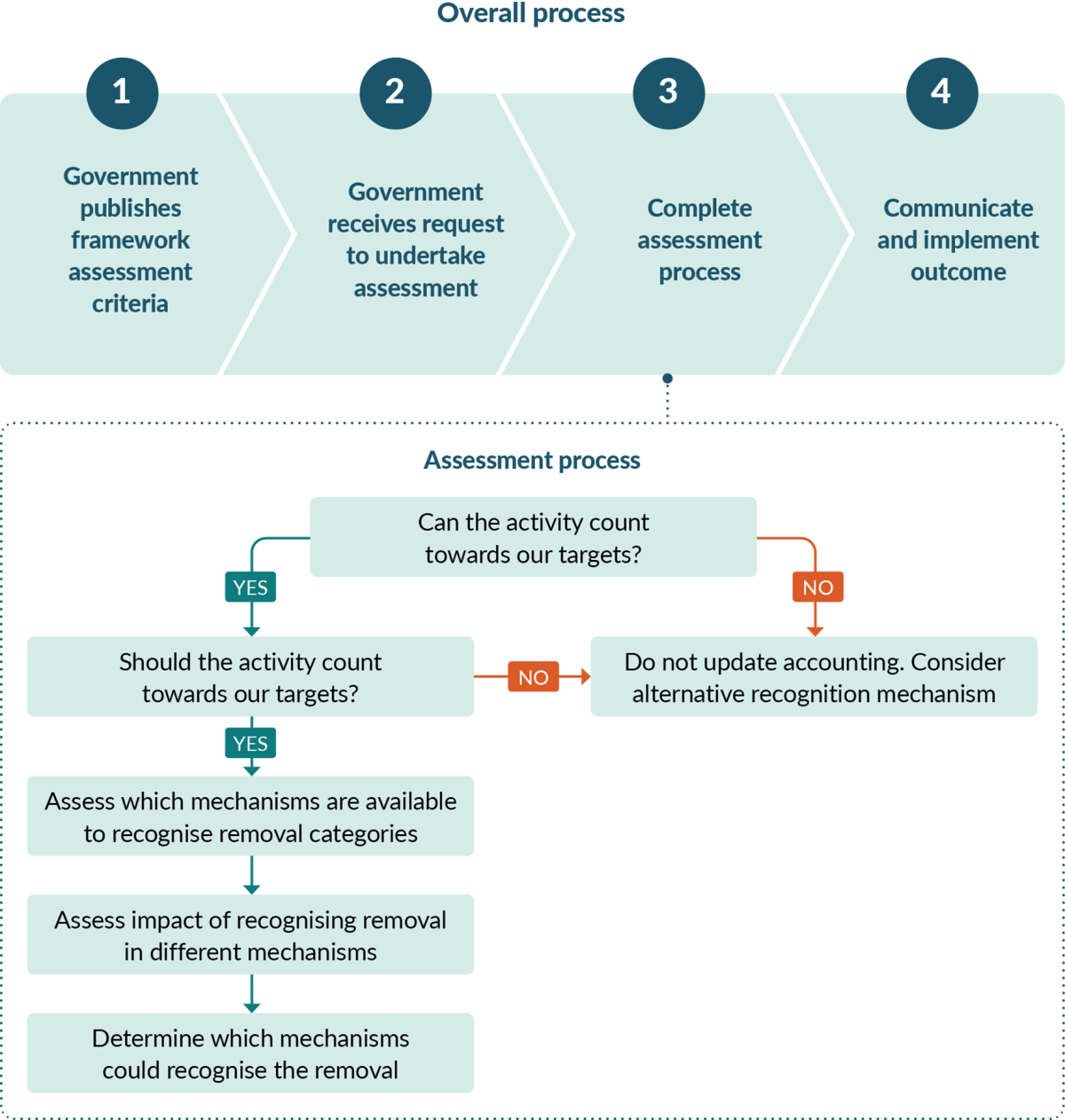

Emissions removals are human-induced activities that draw carbon dioxide from the air or ocean and store it in rocks, on land, in ocean reservoirs or in products such as construction materials.

The following are examples of non-forestry removals.

Many activities act as both a sink and a source of emissions. For example, a carbon sink can become a source of emissions if vegetation is removed or if ecosystems are disturbed or degraded.

Some other types of removal include carbon capture and storage (CCS), enhanced rock weathering and biochar.21 These can remove atmospheric carbon and store it on a permanent basis. Chapter 7 has more detail. Other examples are marine ecosystems, carbon mineralisation and ocean fertilisation, and technology-based activities.

21 Biochar is stable, carbon-rich material produced by heating biomass in an oxygen-limited environment. It may be added to soils to improve soil functions, to reduce greenhouse gas emissions from biomass and soils, and for carbon sequestration.

Carbon sequestration can occur through biological, geological, oceanic, chemical and technological processes. Alongside forestry, we will assess other forms of removing emissions that may become viable.

In practice, we will prioritise the most promising technologies, based on affordability, scalability, scientific validation and overseas acceptance.

Factors for recognising these removals include:

Recognising and rewarding non-forestry removals draws a lot of interest – for example, from people restoring local habitats and from farmers improving the sustainability of their land.

The Government is exploring recognition of non-forestry removals in the New Zealand Emissions Trading Scheme (NZ ETS) or another mechanism, which would require changes to the Climate Change Response Act 2002.

Recognising non-forestry removals could be an incentive that rewards businesses or land owners for their efforts. To ensure any scheme remains balanced, the incentive may also need to be paid back if the removals are later lost (eg, when vegetation is cleared). This is the approach that the NZ ETS takes for forestry.

Recognition could also offer more options for land owners and businesses, create incentives to shift to land use or management that reduces net emissions, and offer other co-benefits, such as better water quality, biodiversity and climate resilience from wetlands. Non-forestry removals can also ensure New Zealand is not reliant solely on forestry offsets.

Different removal activities are at different stages of scientific readiness for recognition in New Zealand. Activities such as peatland restoration could be viable now. However, some activities, such as coastal vegetation management, require further international and New Zealand-specific data and evidence before they can be recognised. The Government will prioritise activities that are viable and have maximum impact.

More work is needed to understand the role of non-forestry removals in reaching New Zealand’s domestic and international targets. Compared with forestry, the potential carbon sequestration is likely to be small in the short to medium term. Changes to our national accounting would also be needed so that New Zealand could count any non-forestry removals towards the targets. This would also mean that emissions from these categories would count against the targets, potentially making these harder to meet in the short to medium term.

There is a range of mechanisms that could recognise non-forest removals. We will develop an assessment framework to identify whether removals are ready to be recognised, and to identify any gaps. Work on the assessment criteria is progressing.

The framework will help us assess a category’s readiness for recognition in the NZ ETS or another mechanism. It will provide the private sector with a recognition pathway that will encourage investment, expanding the portfolio of removals. The categories with larger carbon sequestration potential will be prioritised for assessment when they are ready.

There are two criteria for recognising a non-forest removal:

Currently, forestry is the only land-use category that New Zealand counts towards its NDC. Including non-forest land use is likely to represent an increase in ambition, as New Zealand will have to account for both emissions and removals occurring on that land. It will expand opportunities to use removals other than forestry to meet our international targets, in line with other developed countries.

We will evaluate the best approach to expanding the NDC to include non-forest categories before inclusion in a market system, protecting the integrity of the system. We will use criteria such as: the category meets the Paris Agreement principles; it is supported by strong science; and it meets the minimum Intergovernmental Panel on Climate Change data requirements.

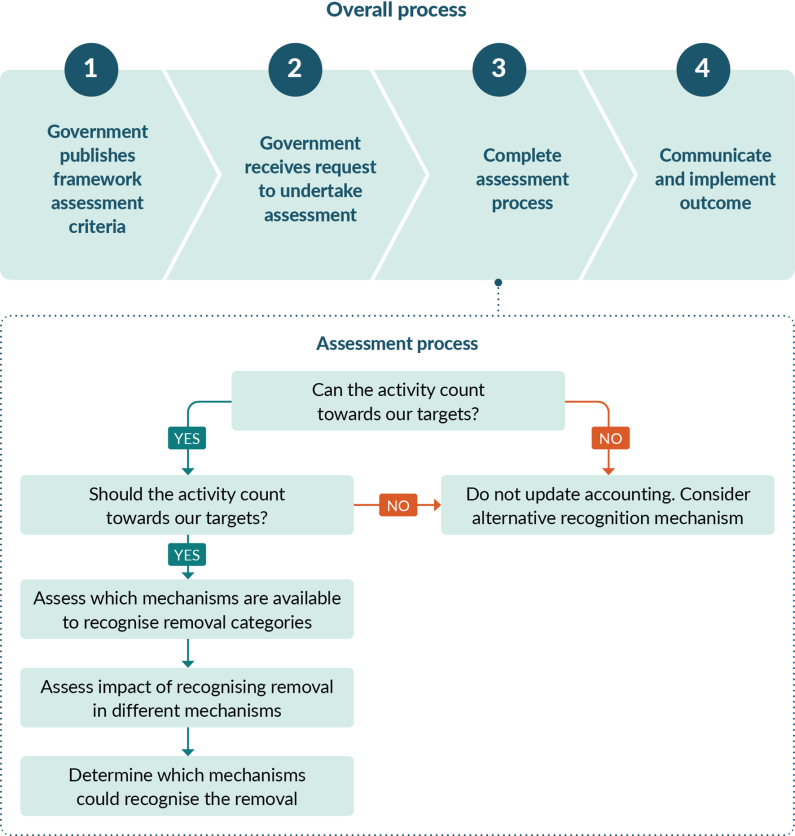

A process for recognising and assessing non-forest removals is set out in figure 12.1.

To assess which mechanisms could recognise a removal category, an impact analysis will determine the costs and benefits. This will include the volume of removals that could be generated, the cost to participants and the Government, and the impact on market credibility and on iwi and Māori.

This will include assessing which mechanisms, other than the NZ ETS, are available to recognise removal categories. Some potential mechanisms need further policy work.

The Government will then decide whether to recognise the removal category:

Officials will then work towards implementing the recognition in the appropriate mechanisms.

| Lead Minister |

|

| Why this sector is important |

|

| Pillars of New Zealand’s Climate Strategy |

|

| Key actions and policies |

|

| Contribution during the second emissions budget period |

|

| Is the sector covered by the New Zealand Emissions Trading Scheme? |

|

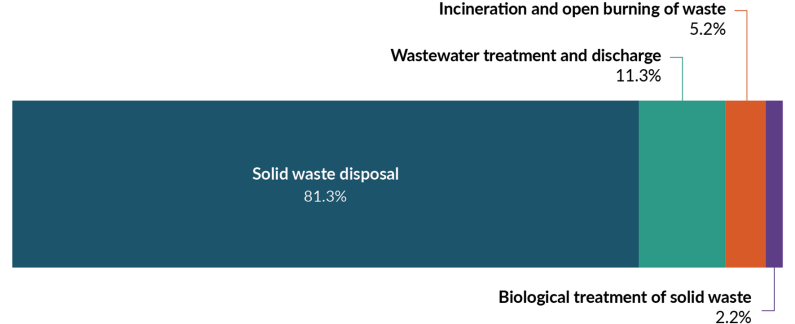

In 2022, the waste sector produced an estimated 3.5 Mt CO2-e (about 4.5 per cent) of New Zealand’s gross greenhouse gas emissions. Waste emissions were comprised of methane (93.3 per cent), nitrous oxide (4.3 per cent) and carbon dioxide (2.4 per cent). Figure 13.1 shows the proportion of emissions by activity.

Waste is an important issue to New Zealanders. By reducing waste, we can also reduce its emissions. Initiatives for the second emissions reduction plan focus on biogenic methane, because it is the main greenhouse gas produced by waste disposal.

New Zealand has a waste disposal levy that is paid on each tonne of waste sent to most landfills in the country.22 The revenue is reinvested through the Waste Minimisation Fund (WMF) and through an allocation to territorial authorities (councils) to invest in local and regional waste minimisation solutions. Since 2022, the WMF has supported infrastructure projects that divert organic materials from landfill, process organic waste or otherwise improve resource recovery, particularly for organics.

New Zealand has a deficit in resource recovery infrastructure23 relative to comparable countries like Australia. Although local government and the waste sector continue to improve waste services, households and businesses still face challenges in recycling unwanted resources that would also help them to reduce emissions.24

The Government has committed to waste minimisation investment priorities (for the WMF) that will also help reduce emissions, including during the second emissions budget (EB2) period. It is assumed a proportion of the WMF will target infrastructure projects and systems that reduce organic waste and emissions (and other waste streams), including those that:

Waste minimisation investments are cost-effective.25 They also offer co-benefits, such as encouraging co-investment from the private sector (commercial projects can contest for WMF funding and require at least 60 per cent as co-funding), and reducing pressure and cost on local government to develop infrastructure, alongside industry and community partners, to meet business and consumer expectations for affordable alternatives to landfill.

22 Excluding class 5 landfills, industrial monofills and farm fills.

23 In 2020, New Zealand had a waste management infrastructure deficit of an estimated $2.1–$2.6 billion. Additional service funding needs amounted to about $0.9 billion. More recent (2024) industry estimates suggest a $4 billion deficit.

24 Waste-related emissions include both disposal emissions (biogenic methane from biodegradable wastes) and the embodied emissions in wasted products and resources. Metals, concrete and plastics have relatively high embodied emissions, but are relatively inert in landfills.

25 Recent waste minimisation investments targeting emissions reductions are forecast to achieve an average abatement of about $30 per tonne of CO2-e across the life of the assets.

In 2004, regulations were introduced requiring landfills that accept municipal waste with a capacity of over 1 million tonnes of waste to capture their emissions.26 Large municipal landfills that meet this threshold have landfill gas (LFG) capture systems. Despite New Zealand’s historically high level of waste per capita, waste emissions have reduced – indicating better management. There may be opportunities to further reduce emissions, including through LFG capture.

26 Resource Management (National Environmental Standards for Air Quality) Regulations 2004. See Ministry for the Environment. National environmental standards for air quality. Retrieved 1 July 2024.